Grayscale research shows that Bitcoin prices are highly correlated with software stocks and have zero correlation with gold. The report’s author, Zach Pandl, points out that Bitcoin has fallen 50% from its October high of $126,000, while gold has surpassed $5,000. This reflects Bitcoin’s deeper integration with traditional finance, driven by institutional participation and ETF activity, but its long-term value storage potential remains optimistic.

Bitcoin’s Correlation with Software Stocks Surges: The Collapse of the Digital Gold Myth

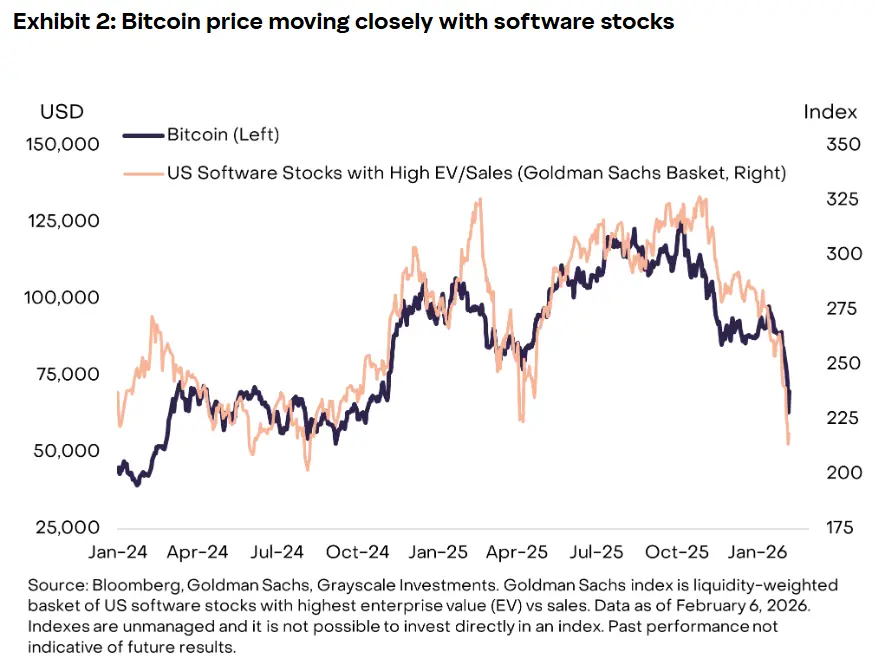

(Source: Grayscale)

According to Grayscale’s latest research, the long-term narrative of Bitcoin as “digital gold” is being challenged, as its recent price movements increasingly resemble those of high-risk growth assets rather than traditional safe havens. On Tuesday, author Zach Pandl stated that although Grayscale remains bullish on Bitcoin due to its fixed supply and independence from central banks, recent market behavior suggests otherwise.

Pandl wrote, “Bitcoin’s short-term price movements are not closely correlated with gold or other precious metals,” noting that gold and silver prices have hit record highs. Gold broke $5,000 per ounce in January, up over 35% from the beginning of the year’s $3,700. Silver surged to $100 per ounce, a more than 230% increase from $30 earlier this year. These trends exemplify safe-haven characteristics: rising counter to market panic.

In stark contrast, Bitcoin’s performance during the same period was entirely different. When Trump announced a 100% tariff increase on China, triggering global market panic, investors sold stocks and cryptocurrencies and flocked to gold. Bitcoin not only failed to serve as a safe haven but also became one of the assets sold off. Similar patterns appeared during the March 2020 pandemic crash and the 2022 Fed rate hike cycle, indicating these are not isolated events but intrinsic to Bitcoin’s market nature.

Grayscale’s charts clearly show that Bitcoin’s recent plunge mirrors the collapse of software stocks since early 2026. When the IGV (iShares Expanded Tech Software ETF) index declines, Bitcoin almost follows the same trajectory and magnitude. This mirror relationship is statistically significant, with correlation coefficients likely exceeding 0.8 (perfect correlation being 1).

Pandl’s core argument is that “Bitcoin’s short-term price movements are not tightly correlated with gold or other precious metals.” This observation challenges the core assumption of Bitcoin as digital gold. If Bitcoin truly were digital gold, it should maintain high correlation with physical gold, rising in tandem during safe-haven demand. Yet, data shows the correlation is near zero or even negative at times.

Grayscale’s Long-Term Defense: Evolution, Not Failure

Grayscale argues that Bitcoin’s recent failure to establish itself as a safe-haven asset should not be seen as a setback but as part of its ongoing development. Pandl states that expecting Bitcoin to replace gold as a monetary asset in such a short period is unrealistic. He notes, “Gold has been used as money for thousands of years, and until the early 1970s, it was the backbone of the international monetary system.”

This defense aims to position Bitcoin as a “growing store of value” rather than a “mature safe-haven asset.” Grayscale’s logic is that gold took millennia to establish its safe-haven status, while Bitcoin, with only 16 years of history, is still evolving. As time progresses and markets mature, Bitcoin may gradually acquire safe-haven properties.

Pandl emphasizes that although Bitcoin has not yet achieved a similar monetary role, the increasing digitization of the global economy through AI, autonomous agents, and tokenized financial markets could steer Bitcoin toward that future. This narrative links Bitcoin to the future of digital economy rather than its past as gold.

Grayscale’s charts show that despite recent poor performance, Bitcoin’s annualized returns over the past decade have significantly outperformed gold. From 2015 to 2025, Bitcoin’s annualized return is approximately 230%, compared to just 8% for gold. This substantial return differential supports its classification as a growth asset rather than a safe haven. Investors buy Bitcoin primarily for capital appreciation, not for preservation during crises.

In the short term, Bitcoin’s recovery may depend on new capital inflows, whether through ETF re-investment or retail investor re-entry. Market maker Wintermute notes that recent retail participation has been concentrated in AI-related stocks and growth concepts, limiting demand for crypto assets. This further confirms Bitcoin’s competitive relationship with growth assets. When retail investors with limited funds choose between AI stocks and Bitcoin, they currently favor the former due to clearer applications and profit models.

From an investment strategy perspective, Grayscale’s research redefines Bitcoin’s role. Investors should view Bitcoin as a growth allocation within their portfolios, not as a safe-haven. This implies that the appropriate allocation to Bitcoin should be comparable to technology stocks, not gold. In risk management terms, holding Bitcoin does not hedge against stock market declines and may even amplify overall portfolio volatility.

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.

Related Articles

U.S. financial regulators bypass Basel Accords to promote the development of tokenized securities, with several major financial institutions launching pilot programs

The U.S. financial regulatory agencies led by Trump are bypassing the Basel Accords to promote the development of tokenized securities, believing that technology-neutral regulatory strategies should be provided. Several financial institutions have taken this opportunity to initiate related pilot projects.

GateNews54m ago

BlackRock, Blackstone, and several other US private credit funds face redemption pressures, triggering liquidity limits

Multiple US private credit funds face redemption pressures in the first quarter of 2026, with funds such as BlackRock, Blackstone, and Blue Owl receiving large redemption requests that exceed the limit, leading to adjustments in buyback policies. Fitch data shows that the redemption rate for perpetual non-listed BDCs has risen significantly, and institutional demand for credit ETFs has surged for protection. S&P Global notes that multiple factors will impact credit market liquidity in 2026.

GateNews1h ago

Saudi Aramco stock price rises 4.3%, the largest increase since April 2023

Gate News: On March 8, Saudi Aramco (the world's largest oil company) stock price increased by 4.3%, marking the largest gain since April 2023.

GateNews1h ago

Starting today, North America observes daylight saving time, and the US and Canadian financial markets' trading hours are moved up by one hour.

Gate News Announcement: On March 8, North America begins Daylight Saving Time today (March 8). The trading hours for financial markets in the US and Canada and the release times of economic data will be one hour earlier than during Standard Time. Specifically, gold, silver, and crude oil will open at 6:00 Beijing time, and US stocks will open at 21:30 Beijing time.

GateNews2h ago

Hyperliquid crude oil products are trading at a premium of over 4% compared to traditional markets, with the on-chain market absorbing the weekend production cut news.

Affected by Middle East production cuts, Brent and WTI crude oil show significant premiums on the Hyperliquid platform, reaching 4.76% and 5.42% respectively. Similar situations were observed in on-chain gold prices during the US-Iran conflict, so investors should exercise caution to handle potential sharp fluctuations.

GateNews2h ago

Bitcoin spot ETF saw a net outflow of $349 million yesterday, with none of the twelve ETFs experiencing net inflows.

On March 7th, Bitcoin spot ETFs experienced a total net outflow of $349 million, with none of the twelve ETFs showing net inflows. Fidelity FBTC and BlackRock IBIT had net outflows of $159 million and $143 million respectively. Currently, the total net asset value of Bitcoin spot ETFs is $87.075 billion.

GateNews3h ago