Trade

Basic

Futures

Futures

Hundreds of contracts settled in USDT or BTC

Options

HOT

Trade European-style vanilla options

Unified Account

Maximize your capital efficiency

Demo Trading

Futures Kickoff

Get prepared for your futures trading

Futures Events

Participate in events to win generous rewards

Demo Trading

Use virtual funds to experience risk-free trading

Earn

Launch

CandyDrop

Collect candies to earn airdrops

Launchpool

Quick staking, earn potential new tokens

HODLer Airdrop

Hold GT and get massive airdrops for free

Launchpad

Be early to the next big token project

Alpha Points

NEW

Trade on-chain assets and enjoy airdrop rewards!

Futures Points

NEW

Earn futures points and claim airdrop rewards

Investment

Simple Earn

Earn interests with idle tokens

Auto-Invest

Auto-invest on a regular basis

Dual Investment

Buy low and sell high to take profits from price fluctuations

Soft Staking

Earn rewards with flexible staking

Crypto Loan

0 Fees

Pledge one crypto to borrow another

Lending Center

One-stop lending hub

VIP Wealth Hub

Customized wealth management empowers your assets growth

Private Wealth Management

Customized asset management to grow your digital assets

Quant Fund

Top asset management team helps you profit without hassle

Staking

Stake cryptos to earn in PoS products

Smart Leverage

NEW

No forced liquidation before maturity, worry-free leveraged gains

GUSD Minting

Use USDT/USDC to mint GUSD for treasury-level yields

More

Promotions

Activity Center

Join activities and win big cash prizes and exclusive merch

Referral

20 USDT

Earn 40% commission or up to 500 USDT rewards

Announcements

Announcements of new listings, activities, upgrades, etc

Gate Blog

Crypto industry articles

VIP Services

Huge fee discounts

Proof of Reserves

Gate promises 100% proof of reserves

Multicoin Capital: Why do we believe stablecoins will become FinTech 4.0?

13m ago

Huang Renxun announced: Generative AI is not truly underway yet; the next phase is the key!

1h ago

Trending Topics

View More14.53K Popularity

572.47K Popularity

69.58K Popularity

4.21K Popularity

4.26K Popularity

Hot Gate Fun

View More- MC:$3.64KHolders:10.00%

- MC:$3.64KHolders:10.00%

- MC:$3.68KHolders:20.04%

- MC:$3.66KHolders:10.00%

- MC:$3.71KHolders:20.00%

Pin

USDT negative premium, holding stablecoins still losing money, how should we respond?

Author: @Web3Mario

Summary: Hello everyone, long time no see. Sorry for the delay in updates; I have been working on designing and developing an AI product for the past three months. Honestly, shifting directions is not easy—any innovation must be built upon clear boundaries within the relevant industry before making incremental breakthroughs. This requires acquiring a lot of foundational knowledge in AI. Now that the product is preliminarily completed, I have more time to discuss macro environments and share my observations on Web3. Today, I want to talk about an interesting topic: USDT negative premium, the continuous strengthening of the RMB, how we should view this, and how to respond. Overall, I believe everyone need not panic excessively. When building your investment portfolio, it’s wise to keep a certain proportion of stablecoin assets, but you can also hedge against exchange rate fluctuations on-chain to avoid some currency conversion losses.

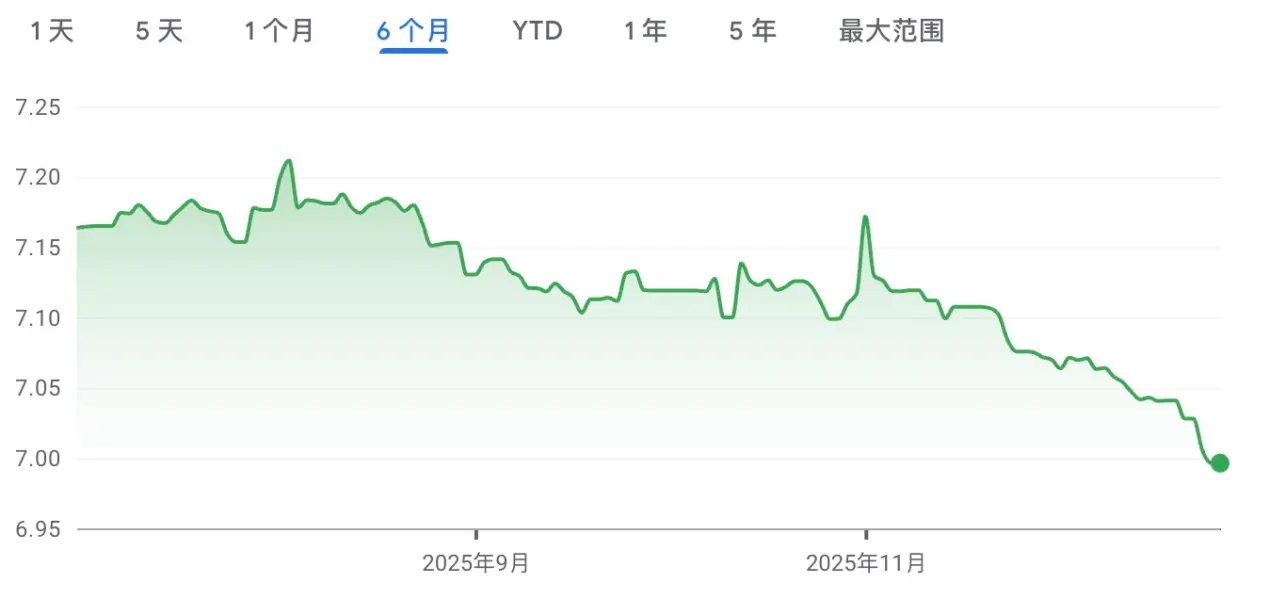

Why is the RMB entering an appreciation phase, and why does USDT show a negative premium?

First, I want to discuss why the RMB is currently appreciating. To understand this, let’s revisit a fundamental economic concept: GDP. Generally, we consider GDP—despite some shortcomings—as the simplest and most effective indicator for assessing a country’s overall economic condition. The GDP composition is:

GDP = C + I + G + (X–M)

Where:

With this simple formula in mind, the reasons for RMB appreciation become clearer, mainly three:

1. Attracting foreign investment and boosting investment expenditure

The first benefit of RMB appreciation is the rapid attraction of foreign capital inflows. We know that in recent times, both China and the US face similar issues—debt problems. The US’s issue is reflected in the explicit federal debt, i.e., the national debt scale, while China’s is mainly in the implicit debt of local governments. Since US Treasuries are tradable and held by a high proportion of foreign investors, debt pressure is greater because default risks are quickly reflected in bond prices through the secondary market, affecting the US’s refinancing ability. Therefore, only through dollar depreciation can dollar-denominated debt’s real value to foreign creditors decrease—this is a form of “inflation tax,” reducing the nominal debt’s real value via rate cuts and quantitative easing. Conversely, China’s local debt is mostly domestic, held by commercial banks or investors, and can be alleviated through measures like debt rollover or transfer payments, so RMB exchange rate pressure from debt issues is less intense. However, this debt issue impacts both countries by limiting government borrowing capacity—meaning expanding government spending to boost GDP becomes more difficult. At this stage, RMB appreciation can help attract capital back into the country.

2. Boost consumption and increase consumer expenditure

Another benefit of RMB appreciation is that it makes imported foreign goods cheaper for domestic consumers, which has two effects: first, it allows ordinary consumers to have more money for consumption and investment, especially in essential goods like food and energy, which constitute the largest share of total consumption. I believe that in the near future, most people will see more imported products on supermarket shelves, and prices will become more affordable. Second, it reduces costs for companies importing raw materials or key components, increasing profit margins, and enabling more capital for expansion and profit distribution.

3. Ease political frictions from international trade and reduce government expenditure

Since China’s trade surplus exceeded $1 trillion in November, there has been increased international discussion about RMB undervaluation. China’s trade negotiations with major export countries, especially the EU, have become more contentious. Why?

Theoretically, in accounting principles, the global current account sum is zero because a country’s exports are another’s imports, and income/transfer payments are reciprocally linked. When trade surplus hits new highs, it implies that some net-importing countries’ deficits are also rising. In the current macroeconomic environment, countries prioritize economic stimulation, so expanding trade deficits can drag down GDP growth—especially for developed countries already experiencing low growth, where small fluctuations can significantly impact GDP. To address trade deficits, two main methods are used: first, protectionism via tariffs, and second, exchange rate adjustments. The US-China tariff truce has paused the first, and RMB orderly appreciation can help quickly ease trade frictions and reduce associated government spending.

While RMB appreciation offers these benefits, it must be stable and orderly—rapid appreciation is problematic. Over the past month, RMB has appreciated notably fast, partly because, by year-end, the GDP growth target for the first three quarters (5.2%) has been largely achieved against the full-year target (~5%). Slightly loosening RMB appreciation helps prepare for next year’s economic transition, monitor market developments, and identify opportunities and risks early. Otherwise, with large foreign exchange reserves, the central bank can stabilize the exchange rate more easily.

I believe that next year, the pace of RMB appreciation will slow significantly, because although the contribution of net exports to China’s GDP is converging, it remains crucial. Rapid appreciation would sharply reduce net exports, putting pressure on next year’s economic growth target.

Having understood the short-term reasons for RMB appreciation, let’s discuss why USDT shows a negative premium. I think there are three main reasons:

In summary, I believe USDT’s negative premium won’t last long. It’s mainly driven by short-term supply and demand shifts. However, the strong RMB in the short to medium term will cause RMB-based investors to face some exchange rate losses.

Should we convert USD stablecoins back to RMB?

Since RMB is appreciating, should we convert USD stablecoins back to RMB to avoid exchange rate losses? I think, unless your portfolio has a very high proportion of USD stablecoins, you can adjust accordingly. Otherwise, maintaining some stablecoin assets is advisable. Three reasons:

1. Exchange losses from USDT negative premium are short-term: As previously explained, I see the negative premium as a short-term phenomenon rather than a structural risk. Converting now could incur significant exchange losses. If you want to adjust your portfolio, it’s better to wait until the negative premium mean reverts before acting.

2. Opportunity cost: While China’s overall economic fundamentals show resilience, challenges remain—particularly the decline in real estate prices leading to a loss of wealth effects across society. Under this context, economic policies focus on stability, debt resolution, industrial restructuring, and redistribution. Although the Chinese stock market has recently rallied, I see this as valuation repair or speculation, not a clear positive for long-term growth. Meanwhile, RMB government bond yields continue to decline, increasing the opportunity cost of holding stablecoins. Holding stable assets offers more flexibility for global asset allocation, especially during the US rate-cut cycle with ample liquidity.

3. Uncertainty of RMB appreciation: US-China tariff tensions are not permanently resolved—they are only paused for a year. The US cannot respond to rare earths immediately and will soon enter a mid-term election cycle, which may lead to a pause and internal focus. But this doesn’t mean tariffs won’t reignite; past analyses of Trump’s policies suggest that before key manufacturing industries return, tariffs could re-escalate, impacting RMB exchange rates.

How to hedge exchange rate losses on-chain, and the role of gold and euro stablecoins

Given this, how can we hedge RMB appreciation-driven exchange rate risks on-chain? The first idea is to use derivatives—like FX derivatives—to hedge. But on-chain, this is very difficult. Last year, I considered creating a decentralized FX derivatives platform to preemptively address this need. However, research showed that related competitors, like DYDX’s Foreign derivatives, have shallow order books and low liquidity, indicating limited market interest—mainly due to regulatory pressures. FX controls are a key tool for manufacturing countries like China, Korea, etc. Therefore, FX derivatives face higher regulatory hurdles, and investors with hedging needs are mostly from these countries, making adoption challenging.

But that doesn’t mean there’s no way to mitigate. I believe three asset classes are worth focusing on:

HKD, JPY, KRW stablecoins: In mid-year, with the US passing stablecoin legislation, many countries launched their own stablecoins. The HKD’s special status and East Asian countries’ overlapping industrial structures tend to align exchange rate trends. Investing in these stablecoins can somewhat mitigate RMB appreciation risks, but recent concerns over regulatory tightening mean we should only monitor until mature products emerge.

On-chain gold RWA: Gold prices have surged in recent years, driven by geopolitical uncertainties and dollar depreciation expectations. For on-chain investors, buying gold RWA tokens like Tether Gold or Pax Gold is relatively easy and liquid. But debates about gold bubbles persist, and recent volatile metal prices suggest the market is in a delicate state. For risk-averse investors without early exposure, holding off might be safer.

Euro stablecoins: I believe euro stablecoins are the most promising among these three. Circle’s EURC is large and liquid. The EUR/USD exchange rate tends to be more stable than USD/CNY, for reasons including China’s export structure—mainly to the EU and ASEAN. China’s exports to the EU are high-margin industrial goods, making EUR a key trade settlement currency. To enhance Chinese goods’ competitiveness in Europe, RMB/EUR exchange rate should stay relatively low.

Of course, exchange rate risks also involve managing political frictions with the EU. Most EU countries are developed, with manufacturing accounting for a higher share of GDP (about 15%) than the US (less than 10%). This means wages and income are more sensitive to capital gains than investment returns. Recently, due to loss of Russian energy supplies, costs rose, impacting manufacturing—especially the automotive sector, a pillar of European industry. This reduces overall industry profits, government tax revenue, and slows wage growth, affecting welfare and consumption. Europe’s capital competitiveness in AI has also declined, with capital flowing to US AI markets for higher returns. Investment outlook is cautious. As a result, net exports’ impact on the economy is amplified, and European governments are more aggressive about trade deficits.

However, I believe the EU does not have the same strategic bargaining capacity as the US in the trade war, nor is there consensus among EU countries—Hungary, Spain, etc.—making negotiations complex. I think China and the EU will not significantly adjust exchange rates for trade rebalancing but will focus on EU profit-sharing and investment agreements as the main cooperation framework. European capital markets are more mature than those in emerging markets like India, Vietnam, Brazil, etc., offering better capital protection. China’s ample FX reserves can be reinvested to boost profits. Stable exchange rates also help Chinese goods remain competitive in Europe.

Returning to on-chain hedging, a practical approach is to convert USD stablecoins into EURC, then deposit them on platforms like AAVE to earn interest—current utilization rates offer around 3.87% yield, which is attractive. If you want exposure to risk assets like BTC while hedging FX risk, you can use EURC as collateral to borrow USD stablecoins and then allocate assets, such as buying BTC.