The competition of stablecoins is essentially a comprehensive game of compliance capability, technological efficiency, yield innovation, and globalization strategy.

Written by: MaoSphere

According to the stablecoin status report jointly published by Dune and Artemis, as of February 2025, the global stablecoin supply has reached 214 billion USD, with annual transfer volume exceeding 35 trillion USD, far surpassing Visa. The number of active addresses surged by 53%, with significant institutional funds pouring in, driving the integration of traditional finance and the crypto market. Decentralized stablecoins like USDe and USDS have rapidly risen, becoming the third-largest and an emerging important stablecoin, respectively, while USDC has doubled its market value to 56 billion USD due to regulatory benefits and partnerships with giants. USDT’s market share has declined, shifting towards the P2P remittance sector, with a total market value growth to 146 billion USD, still the largest stablecoin by market value. Both remain in an undisputed leadership position. Today, we will analyze these two projects.

Tether

The Tether official FAQ states that “all Tether tokens are pegged 1:1 to the corresponding fiat currency (for example, 1 USDT = 1 dollar), and are 100% backed by Tether’s reserves.” Therefore, Tether is a fiat-collateralized stablecoin, currently offering five types of stablecoins pegged to different fiat currencies and commodities: USDT (dollar), EURT (euro), CNHT (Renminbi), MXNT (Mexican Peso), and XAUT (gold).

Tether was founded in July 2014 by Brock Pierce, Craig Sellars, and Reeve Collins, initially named “Realcoin,” and is a stablecoin designed to maintain a fixed 1:1 exchange ratio with the US Dollar (USD). As one of the earliest created stablecoins, it is built on Mastercoin (Omni), a protocol layer of Bitcoin. The first tokens were issued on Omni in October 2014 and were renamed “Tether” in November 2014, pioneering the fiat-backed stablecoin model and achieving the most widespread trading. Tether’s fiat-collateralized tokens are digital assets issued on various blockchains. Each issued and circulating Tether token is backed by assets (“reserves”) held by Tether and its affiliates, with reserve reports released quarterly.

Structurally, as of December 31, 2024, Tether Holdings Limited was also a company in the British Virgin Islands. Tether Limited is one of the members of the group and has registered as a money services business with the Financial Crimes Enforcement Network of the U.S. Department of the Treasury. As of December 31, 2024, the group members submitted reports to the British Virgin Islands Financial Investigation Agency in accordance with applicable laws. Certain members of the group successfully migrated from the British Virgin Islands to El Salvador in January 2025. Tether International S.A. de C.V. became the sole issuer of currency-pegged tokens. Tether International S.A. de C.V. has been authorized as a stablecoin issuer and digital asset service provider under the El Salvador Digital Assets Issuance Law and is subject to regulatory requirements set forth by the National Commission of Digital Assets of El Salvador. TG Commodities S.A. de C.V. has been authorized as a stablecoin issuer and digital asset service provider under the El Salvador Digital Assets Issuance Law and is subject to regulatory requirements set forth by the National Commission of Digital Assets of El Salvador. Currently, El Salvador is rapidly emerging as a global hub for digital assets and technological innovation, attempting to leverage its forward-looking policies, favorable regulatory environment, and growing Bitcoin professional community. By embracing blockchain technology and digital currencies, El Salvador is fostering an ecosystem that encourages innovation and attracts broader investments in the financial and technological sectors. The Salvadoran government has even planned a “Bitcoin City” economic zone aimed at creating a tax-free, energy self-sufficient future city, primarily supported by geothermal energy for Bitcoin mining.

Tether’s technology stack has three layers, each with many functions:

- The first layer is the native blockchain. Tether uses the native transaction system of each blockchain to support the tokenization system of that blockchain.

- The second layer is the tokenization system of the blockchain. Each blockchain’s tokenization system allows Tether to track and report the circulation of Tether tokens; and enables users to transact and store Tether tokens and other assets/tokens in a peer-to-peer, pseudo-anonymous, cryptographically secure environment; in supported blockchain wallets/software; and in systems that support multi-signature and offline cold storage.

- The third layer is the Tether Group, where different business entities within the group are responsible for accepting fiat currency deposits and issuing corresponding Tether tokens; processing fiat currency withdrawals and redeeming corresponding Tether tokens; publicly reporting reserve proofs; and operating the Tether website (which allows eligible KYC-verified customers to directly purchase and redeem Tether tokens from Tether at a fixed exchange rate of 1:1, minus fees).

Tether has a diverse user base, and the reasons individuals use Tether vary. This includes traders seeking daily profits; long-term holders looking for secure storage of their digital assets; those wanting to make global payments more freely, quickly, and cheaply; individuals in developing countries seeking to access financial services for the first time or looking for a store of value in an environment where local currencies are depreciating or unstable; and developers seeking to create new technologies. For merchants, allowing them to price goods in fiat currency value instead of digital assets (with stable conversion rates/purchase windows) eliminates intermediaries. For exchanges, it also addresses the complexities, high risks, slowness, and costs associated with accepting fiat currency deposits and withdrawals through traditional financial systems. Thus, in 2024, Tether’s net profit reached $13.7 billion, with income derived from transaction fees and reserve investment returns. Tether invests the dollar reserves deposited by users into short-term U.S. Treasury bonds and other highly liquid assets, achieving profitability through interest rate spreads (and the cost of funds is zero!). [1].

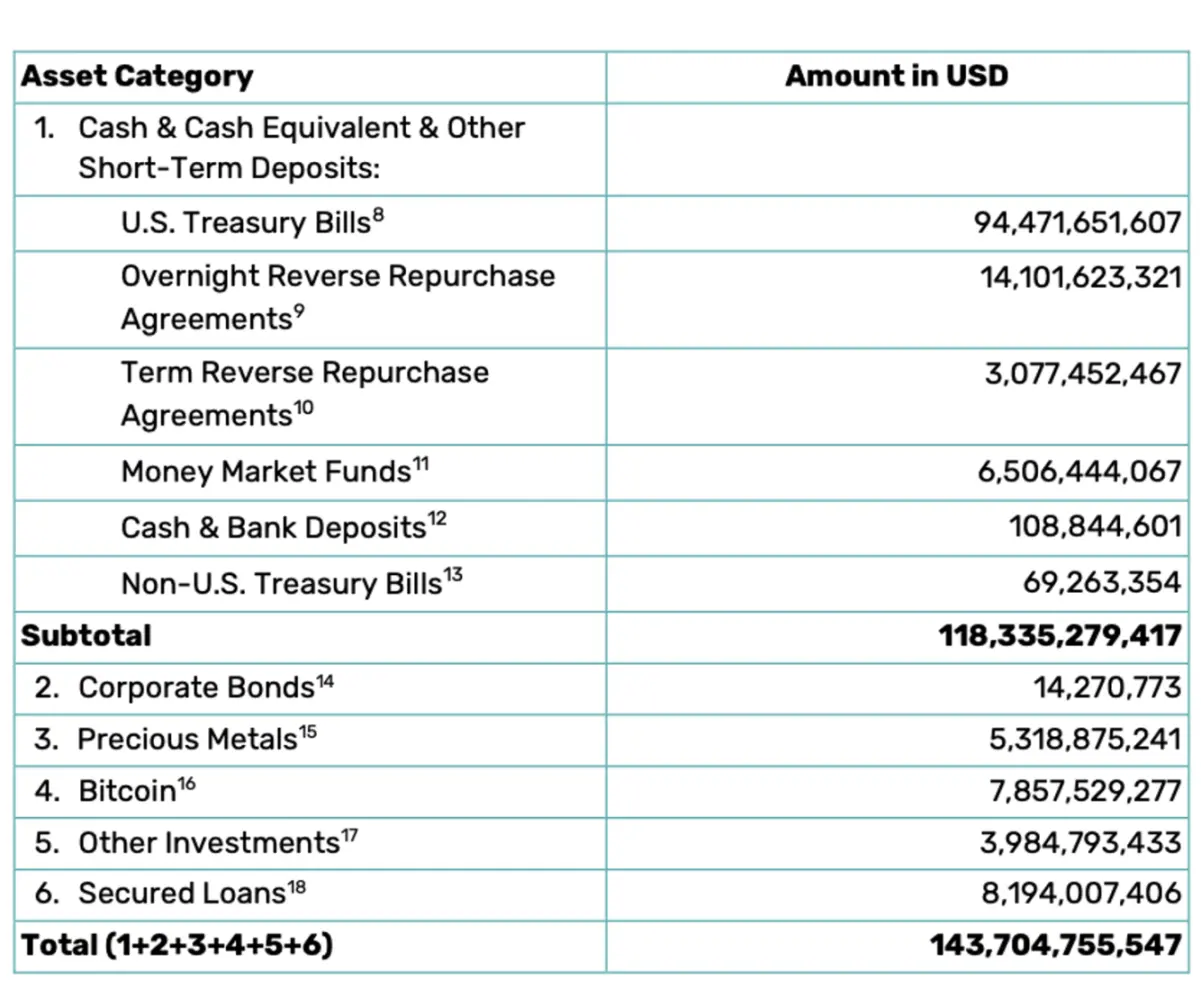

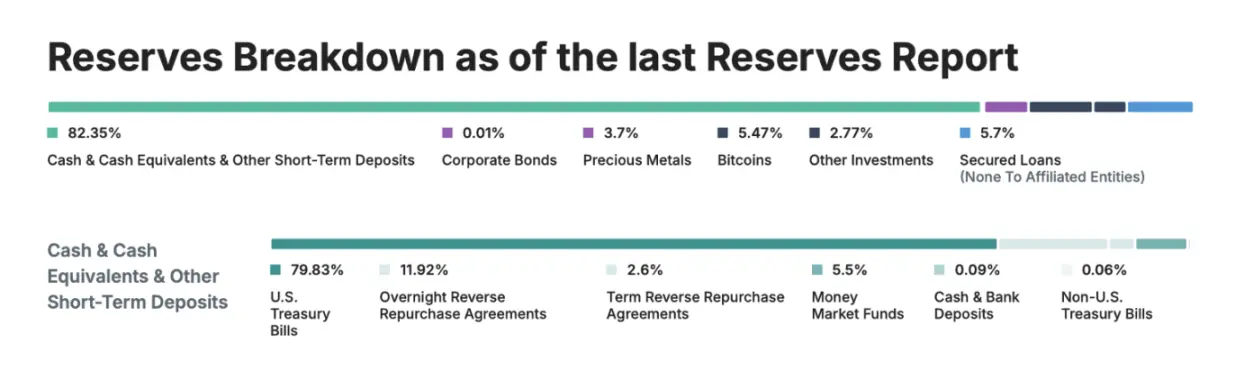

According to the data audited by BDO as of December 31, 2024, the structure of the collateralized assets is roughly as follows (including only the issuer Tether International Limited (BVI) and Tether Limited (HK)). A major highlight of this quarter is Tether’s increased exposure to U.S. Treasury bonds, surpassing major economies such as Germany and the UAE, making Tether one of the largest holders of U.S. Treasury bonds globally. These holdings provide crucial liquidity and strength to the U.S. debt market and indirectly enhance global confidence in the stability of the U.S. dollar.

At the end of this record-breaking year for Tether, its CEO Paolo Ardoino stated:

“Tether’s certification opinion for the fourth quarter of 2024 further solidifies our global leadership in financial transparency, liquidity, and innovation. Holding over $113 billion in U.S. Treasury securities and with a reserve buffer exceeding $7 billion, Tether continues to set the gold standard for stability and trust in the digital asset space with $45 billion in new issued tokens throughout the year. The group’s equity exceeds $20 billion. Our licensing milestone in El Salvador and investments in transformative sectors further underscore our steadfast commitment to promoting financial inclusion and resilience.”

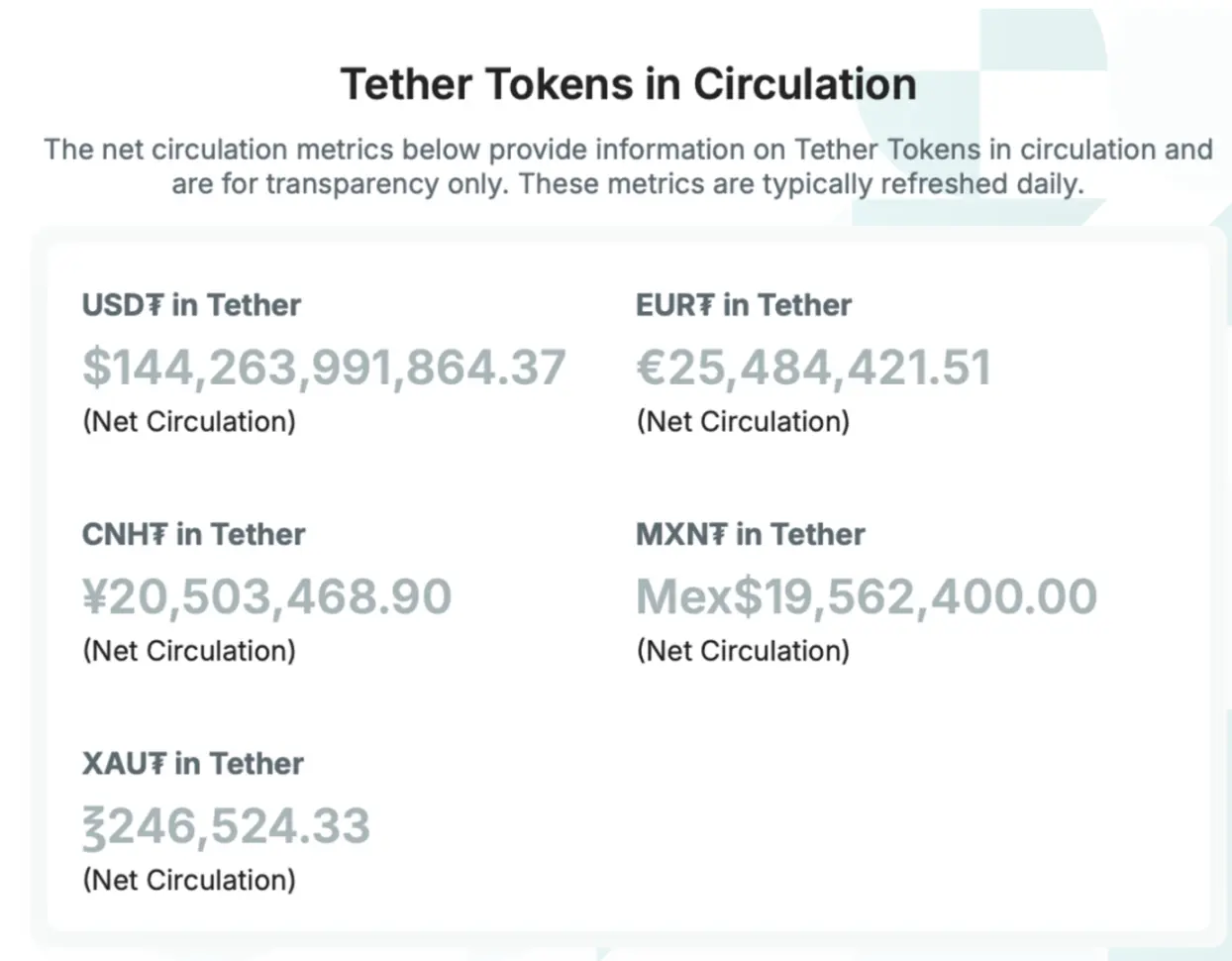

As of January 22, 2025, Tether has 882 customers. The minimum purchase amount for Tether tokens through the Tether website is $100,000, and currently, a fee of 0.1% or $1,000 (redemption) and 0.1% (purchase) is required for buying Tether tokens through the Tether website, of course, this requires going through the KYC process. Tether tokens can also be bought and sold on the secondary market, including exchanges and over-the-counter platforms that support Tether tokens outside of El Salvador, such as Binance, OKX, Coinbase, Kraken, etc. Users can also trade and store Tether tokens using any supported blockchain wallet. As of the date of this publication, its circulation is still increasing:

In March of this year, Tether announced the appointment of Simon McWilliams as CFO, marking an important step in the company’s historic move towards a comprehensive financial audit. This new CFO will lead Tether’s further commitment to transparency and regulatory readiness. With his appointment, Tether is firmly committed to completing a full audit, which is a key step in raising industry standards and strengthening regulatory engagement. Although Tether has already set a benchmark for stablecoin transparency through BDO’s quarterly certifications, the comprehensive audit will ensure greater financial integrity and reserve verification. The audit is a critical step in Tether’s broader strategy, aimed at expanding its influence within the institutional financial system. As demand for dollar-backed assets continues to grow, Tether has become the largest digital channel for accessing dollars, benefiting over 400 million users globally, especially in emerging markets and among unbanked populations overlooked by the banking industry. In addition, from its strategic investments, we can also see its inclination to diversify its portfolio by investing across multiple industries, including:

- Complete a strategic investment in Zengo Wallet. Zengo Wallet is a leading self-custody cryptocurrency wallet known for its focus on security and ease of use. This investment underscores Tether’s commitment to advancing secure self-custody solutions and promoting the global adoption of stablecoins.

- On March 27, 2025, Tether announced a strategic investment in Be Water. Be Water is an innovative media company focused on the production and distribution of audio, video, film, and live content. Through a capital increase and equity acquisition of 10 million euros, Tether will acquire 30.4% of Be Water’s shares by the end of this month. With this investment, Tether and Be Water will collaborate to enhance digital content distribution, integrate new technological solutions, and support Be Water’s international brand expansion.

- Investment of $775 million in the video platform Rumble

- Strategic minority stake in Juventus Football Club, and

- A $200 million investment in Blackrock Neurotech, a company focused on brain-computer interface technology.

These measures demonstrate Tether’s commitment to driving technological innovation across multiple industries.

USDC

USDT dominates P2P payments and exchange liquidity in emerging markets in Asia, while USDC is more used in compliance financial scenarios in Europe and the US (such as cross-border remittances and institutional DeFi). As the second largest stablecoin by market capitalization, it serves as a model for embracing regulation. Next, let’s talk about USDC.

Although it was born relatively late, USDC has had a tumultuous history. On May 15, 2018, Circle announced USDC, which was officially launched by Centre in September of the same year. Centre is an alliance co-founded by Circle and Coinbase, and later, on March 29, 2021, Visa announced its support for USDC, allowing it to be used for sales transactions on Visa’s payment network, gaining significant attention. However, in 2023, we all know that the traditional financial industry’s banking crisis impacted the cryptocurrency world. On March 10, 2023, Silicon Valley Bank (SVB) was forced to close due to insufficient liquidity and insolvency, becoming the second-largest bank failure in U.S. history. Silicon Valley Bank was one of Circle’s six banking partners, managing about 25% of USDC’s cash reserves. On March 11, Circle announced that it had approximately $3.3 billion in USDC reserves at Silicon Valley Bank, accounting for 8% of the total reserves. Due to the bank’s collapse, this portion of funds was frozen, triggering a crisis of confidence in USDC. Concerns about Circle’s ability to recover the reserves led to panic selling of USDC by investors, causing its price to drop to $0.87 at one point, marking the most severe depegging in history. Panic spread, and many users attempted to exchange USDC for U.S. dollars or other cryptocurrencies, leading to a risk of a run on the USDC redemption system. Some exchanges (such as Coinbase and Binance) suspended the conversion services of USDC to U.S. dollars. Circle promised that if the $3.3 billion in reserves at Silicon Valley Bank could not be returned 100%, it would use company resources and external capital to make up the shortfall. On March 12, U.S. regulators pledged full compensation to Silicon Valley Bank depositors, alleviating Circle’s cash reserve issues. The price of USDC gradually rebounded to around $0.95. This incident also reminded the market that the stability of stablecoins is not absolute and still relies to some extent on the stability of the traditional financial system.

In August 2023, Circle and Coinbase disbanded the Centre consortium, which had been responsible for managing USDC since 2018. Circle acquired Coinbase’s remaining 50% stake in Centre through a $210 million stock purchase, making Centre a wholly-owned subsidiary, and officially disbanded it in December 2023. This move gave Circle full control over the issuance and governance of USDC, including holding all smart contract keys, complying with reserve governance regulations, and enabling USDC on new blockchains, thereby granting Circle complete governance over USDC. This decision is also entirely understandable, as stablecoins face increasingly stringent regulatory scrutiny, particularly following the collapse of TerraUSD and the Silicon Valley Bank incident. Circle aims to meet regulatory requirements through a clearer governance structure. Despite the disbanding of Centre, Circle and Coinbase continue to maintain a close revenue-sharing partnership. Coinbase, by holding equity in Circle, continues to benefit from the USDC reserve income, and the amount of USDC held on its platform directly affects its revenue-sharing proportion.

After everything settles, USDC is currently issued by Circle, a fintech company headquartered in the United States. In the U.S., Circle holds the relevant licenses in all required U.S. jurisdictions. Additionally, Circle holds virtual currency licenses in New York and Louisiana and is registered as a “money services business” with the Financial Crimes Enforcement Network (FinCEN). Besides the licenses obtained in the U.S., it has also acquired a Digital Asset Business (DAB) license in Bermuda, an Electronic Money Institution License in France, a Major Payment Institution License in Singapore, and a Financial Conduct Authority E-Money Issuer License in the United Kingdom.

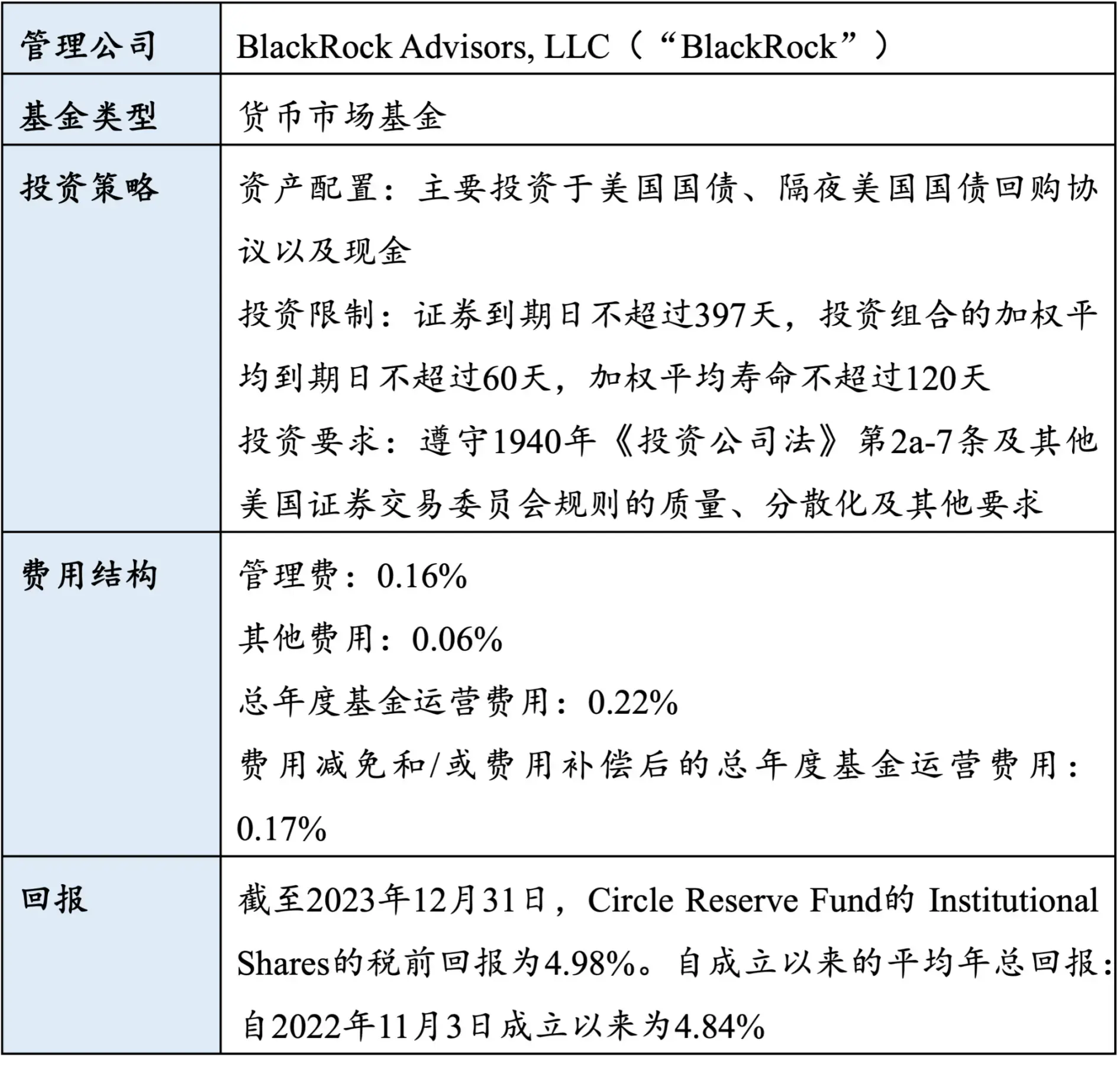

Most of the reserves of USDC are held in the Circle Reserve Fund (USDXX), which is a money market fund established under Section 2a-7 of the Investment Company Act of 1940 (as amended). Through BlackRock, the portfolio of the Circle Reserve Fund is reported daily by an independent third party, and these reports are open to the public. To summarize the product prospectus:

Summary

Similar to Tether, Circle’s profit model mainly includes the following aspects:

1 Reserve Earnings: Circle invests the US dollar reserves deposited by users in low-risk assets such as short-term U.S. Treasury bonds and repurchase agreements, generating profits through interest rate differentials. In 2024, Circle will generate $1.7 billion in revenue from reserve assets, of which 50% will be shared with Coinbase.

2 Ecosystem Cooperation: Institutional users need to pay a fee when minting or redeeming USDC through Circle Mint, with rates typically ranging from 0.1% to 0.5%. USDC supports 16 blockchains, and Circle charges transfer fees through cross-chain protocols (such as CCTP), with cross-chain transaction volume exceeding 20 billion USD in 2024. In lending and liquidity mining scenarios on platforms like Compound and Aave, Circle may share transaction fees with protocol parties.

3 Enterprise Services: Circle provides services such as USDC custody and settlement for banks and payment companies, for example, developing digital asset infrastructure in collaboration with JPMorgan. Circle’s compliance tools (such as on-chain monitoring, KYC/AML systems) can be authorized to exchanges or enterprises, charging a technical service fee.

In 2025, Circle launched USYC (tokenized money market fund) after acquiring Hashnote, providing institutions with an annualized return of 3.8%, while also profiting through management fees.

According to the USDC reserve asset details released by Deloitte on March 28, 2025, as of January 31, 2025:

In comparison to the asset allocation on both sides, Tether’s asset allocation is more diversified, including not only U.S. Treasury bonds but also cash and cash equivalents, secured loans, corporate bonds, funds, and precious metals. This diversified allocation may provide Tether with greater stability and risk resistance, but it also increases complexity and potential opacity. In contrast, USDC’s asset allocation is relatively simple, mainly focused on cash and U.S. Treasury bonds, which makes the transparency and stability of its reserve assets easier to verify.

From a development trend perspective, USDT is expanding through local payment channels in Southeast Asia and Latin America, while USDC is promoting merchant scenarios through partnerships with financial institutions in Europe and the United States (such as Mastercard). In terms of compliance and transparency, there are still significant differences between the two. USDC actively embraces U.S. federal regulation, whereas USDT initially relied on offshore structures and has recently expanded into emerging markets through compliance partnerships in Singapore, Hong Kong, and other locations. USDT invests 80% of its funds in short-term U.S. Treasury bonds and reverse repurchase agreements, with an annualized return of approximately 4.5%, supporting its net profit of $13.7 billion in 2024. USDC focuses more on cash and ultra-short-term government bonds, offering higher liquidity but lower returns. However, USDT holds a small amount of corporate bonds and Bitcoin, making its potential volatility higher than that of USDC’s purely cash-type assets.

In terms of Compliance, Circle has consistently implemented its strategy. Circle is the first project to meet the requirements for issuing stablecoins in Canada and has established a company in ADGM to expand into the Middle Eastern market. In 2024, Circle became the first major stablecoin issuer to fully comply with the European Markets in Crypto-Assets (MiCA) regulation. Its CSO stated: “With this progress and with France as our regulatory hub in Europe, USDC and EURC enjoy a passport across the EU — a market of over 445 million consumers that constitutes the world’s third-largest economy. Given the novel global circulation of stablecoins, Circle collaborates with regulatory and policy stakeholders in France and the EU to ensure the global circulation of USDC and EURC within the EU. This not only provides EU market participants with stablecoins denominated in local currencies but also ensures that dollar activities in the EU are fully regulated. Meanwhile, in the United States, legislative progress in the House and Senate may now find a path to passage under the incoming Trump administration, which has expressed support for growth, innovation, and pro-cryptocurrency policies. This is not a policy effort that the U.S. needs to start from scratch, as there is already a bipartisan framework for establishing rules for U.S. stablecoins and for the structure of the cryptocurrency market. In this context, President Trump has the opportunity to turn his campaign promise of U.S. leadership in the cryptocurrency space into reality. By regulating stablecoins, the U.S. can help ensure that the digital dollar becomes the reserve currency of the internet, just as it is the reserve currency of the world.”

Epilogue

The competition of stablecoins involves multiple complex aspects and requires a comprehensive evaluation from various angles such as technology, finance, regulation, and market. On one hand, market share and trading activity are direct indicators of the dominant position of stablecoins. As of 2024, USDT holds the top position with over 70% market share, and its daily trading volume accounts for 46.85%, far exceeding USDC (21.3%) and DAI (3.39%). On the other hand, supporting more blockchains can enhance liquidity and application scenarios. For example, both USDT and USDC cover mainstream public chains, while the trading volume of USDC on the Solana chain surged due to the meme coin craze. Traditional stablecoins (like USDT and USDC) do not share reserve earnings with users, while interest-bearing stablecoins attract long-term holders through a profit-sharing model, but they need to address the issue of fragmented liquidity.

The competition among stablecoins is essentially a comprehensive game of compliance capabilities, technological efficiency, yield innovation, and globalization strategies. In the future, leading projects (such as USDT and USDC) need to continuously optimize reserve management and expand application scenarios, while emerging forces may seize niche markets through differentiated positioning. The uniformity of regulation and the security of technology will be key variables for the long-term development of the industry. The stablecoin market is expected to deeply integrate into the global financial system between 2025 and 2030, but it may also face challenges from strict regulation and central bank digital currencies (CBDCs).

[footnote]

[1]