Author: Yuan Chuan Investment Commentary

Anthropic’s latest unemployment report sends chills down the spine of financial practitioners.

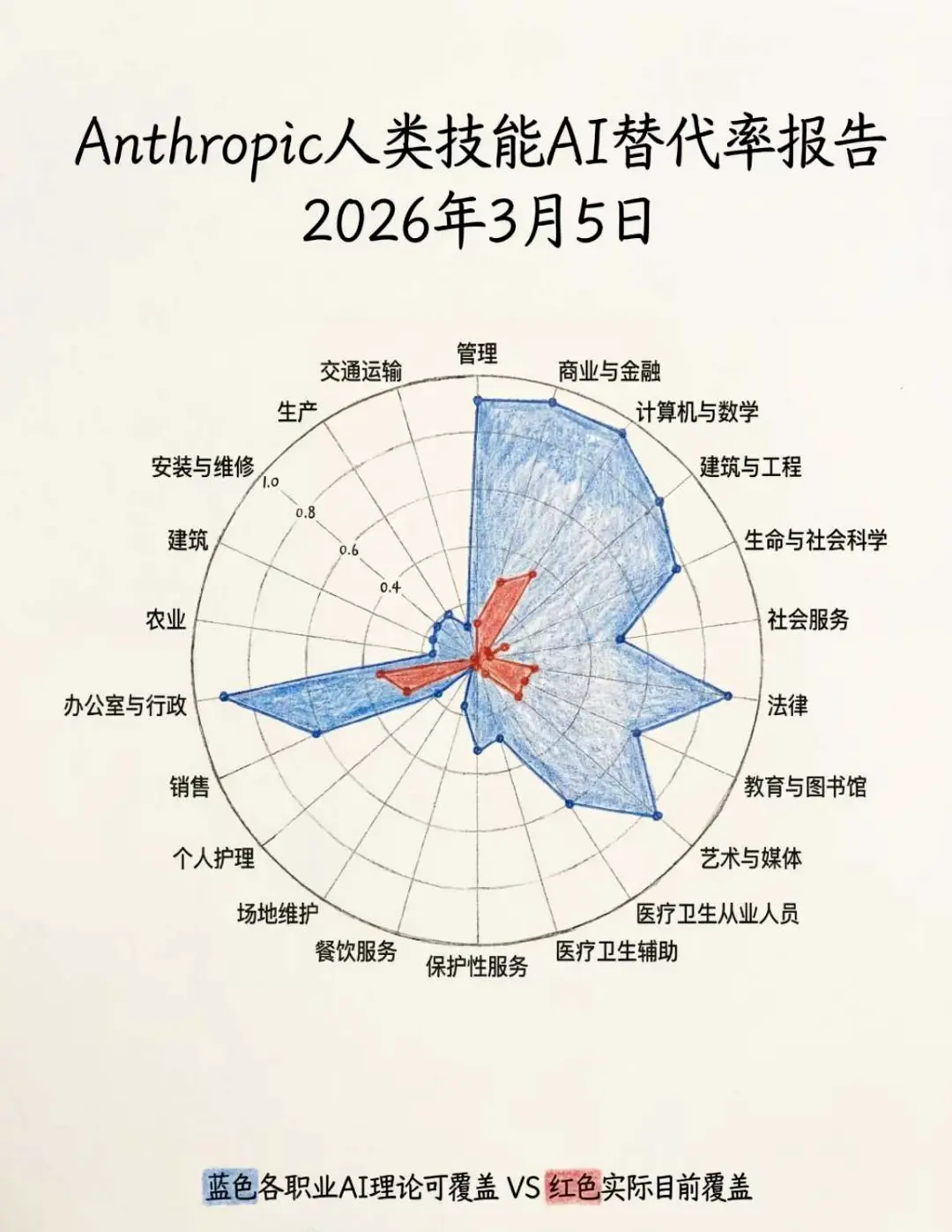

The report states that the replacement rate for financial positions is as high as 94%, ranking second among all professions, but the current actual replacement rate is only 28%, leaving huge room for growth. Fortunately, 30% of jobs are almost unaffected, so financial professionals can consider re-employment opportunities like dishwashers or plumbers.

After working in the industry for a long time, there’s always a sense of anxiety—financial professionals live in a world of “comparisons,” with sales evaluations and performance rankings pressing down daily. As long as they don’t keep learning, a sense of unease will arise.

It’s like after the Spring Festival holiday, returning to the office and still chatting with Chatbot, while the colleague at the next desk has already raised 8 lobsters and is passionately arguing about crude oil price fluctuations.

The financial industry has never rejected efficiency—shifting from manual order entry to algorithmic trading, from offline bank sales to online distribution—all these are driven by the same principle. But this time, AI is replacing not just inefficient financial tools, but the inefficient people behind those tools. After all, the highest cost in finance is human resources. Behind the profits of asset management firms, it’s about how to manage more money with fewer people.

Thus, private equity firms are beginning to embrace advanced productivity: Diewei Asset offers online courses teaching how to tame “digital researchers” working 24/7; Mingxi Capital uses Manus to automatically generate promotional materials for dividend growth, with layouts rivaling high-end magazine aesthetics. Even clients have become more shrewd—after a financial manager just recommended a popular private fund, they immediately ask whether they should buy Doubao.

The private equity industry is gradually entering a “Detroit: Become Human” moment, where every link in the mature chain—research, operations, sales—is beginning to be replaced.

Compensation VS Token Costs

In a competitive environment with rising operating costs and increasing difficulty in alpha generation, efficiency per human is a key metric private equity bosses obsess over before sleep.

In the private equity industry chain, researcher salaries are generally high. According to MuliCube data, stock quantitative researchers earn between 800,000 and 1.5 million yuan annually. Subjective researchers earn slightly less, but sometimes receive shocking incentives—early this year, a top subjective researcher managing hundreds of billions earned over 20 million yuan in year-end bonuses for recommending Nvidia.

If private equity can successfully rely on AI for research and investment, saving millions in costs, and if AI can work 24 hours, reducing hourly wages while increasing output, then travel, overtime, transportation, and meal allowances—expenses that are deducted from the carry—are all money AI doesn’t need.

In asset management, all technological progress boils down to two words: increasing efficiency and reducing costs. Private equity bosses don’t care whether AI can think like humans; they only care whether the work can be done.

Howard Marks calculated that if an analysis produced by an AI assistant earning $200,000 annually is reliable, then for the payers, whether it involves genuine thinking or pattern matching doesn’t matter—the key is whether the work results are dependable enough to be useful.

After the Spring Festival, eight securities firms’ quantitative teams collectively released tutorials on “Lobster Farming,” accelerating the process of replacing human researchers. They personally tested OpenClaw, which can proactively produce research results like humans.

On the entry app, a presentation titled “OpenClaw: From Beginner to Master” has been played 4,839 times; Northeast researcher Xu Jianhua promoted 20 skills that can boost research efficiency tenfold; Fangzheng’s Cao Chunxiao reproduced PB-ROE strategies, cup-and-handle stock selection strategies, and fully automated factor mining and backtesting with lobsters.

Thinking about it deeply, this is equivalent to OTA (Over-The-Air update) of Buffett, O’Neil, and Simmons’ skill sets simultaneously.

Eager Learners in Trading

Sell-side actively popularizes, buy-side learns eagerly. A private fund in Beijing, worried about contamination of their mainframe, gave each researcher a new computer and a 50,000 yuan token subsidy, specifically for lobster farming[1].

Yang Xinbin from Snowball Asset Management has trained two lobster researchers. He says that daily conversations with AI are much more frequent than with humans. The AI agents they develop can do in two days what a mature quantitative researcher might take half a year to accomplish, with even greater potential.

Paul Wu from Qinyuan Investment gradually integrates AI into various departments. He feels that AI can complete closed-loop tasks in some roles and operate independently through iteration. He foresees that soon, the company’s expenses will be just for purchasing and maintaining an Apple analyst AI, and later perhaps a portfolio advisor named Paul.

In the past, many private funds experienced friction in research transformation—researchers felt fund managers were inadequate, and fund managers thought researchers were useless. The emergence of OpenClaw offers private fund bosses a new possibility—no more internal friction with mediocre researchers, nor worries about core researchers being poached by competitors with high salaries.

From a characteristic perspective, lobsters fulfill all the ideal images fund managers have of researchers: working around the clock, no vacations, no loafing; long-term memory retention, key data readily available; absolute loyalty and obedience, no rebellion or factionalism; continuous self-iteration, unlike veteran researchers who get stuck in path dependence and are eventually phased out.

If future silicon-based tokens cost far less than carbon-based salaries, how can private fund bosses refuse a well-behaved, trainable, and cultivatable AI researcher?

Replacement Is Not Just About Lobsters

Subjective private funds are still weighing whether token costs are worthwhile. Large quant firms, relying on self-built infrastructure, have already driven token costs down to very low levels. But they remain surprisingly calm in the face of this trend.

“OpenClaw is just a semi-finished toy for the quant tech circle,” a leading Shanghai quant expert told me. Its significance lies in lowering technical barriers for subjective institutions and retail investors, providing a clear cost recovery path for large model companies’ massive initial infrastructure investments, but it’s not very meaningful in serious quantitative investment environments.

Another top quant expert expressed more bluntly: Lobsters in finance are like a pyramid scheme. OpenClaw has randomness, non-systematic features, and low security, which could introduce huge uncertainties into the entire quant system.

OpenClaw isn’t advanced productivity in the quant world. Cui Yuchun from Xuntu Technology believes there’s no need to worry:

Lobsters are even weaker than Manus and Kimi in agent optimization and tool invocation (including research browsers, writing, data analysis tools). For a researcher without programming background, deploying and launching takes 5-10 hours, and most tasks can’t achieve results above 60 points.

When retail investors use China Stock Analysis Skill to select stocks, it feels like opening a new world. Quantitative systems have built multi-agent platforms, with richer agent libraries, crushing lobsters. However, the operation of this powerful system may not require more humans.

Traditional quant research systems usually follow a pipeline: data cleaning → factor calculation → model prediction → portfolio optimization. In the AI era, some institutions, like top overseas quant firms such as Man Group, are simplifying roles into: role division → tool invocation → workflow design. Standardized, repetitive tasks are gradually replaced by AI agents, reducing the need for many researchers in factor factories.

For example, Xiyue Investment’s Apollo AI multi-agent system embeds AI agents into research, data, trading, and operations. Founder Zhou Xin describes it as having the equivalent of 700-800 AI employees.

With the previous “artificial factory”-like sci-fi dominance in quant, and now retail investors leveraging OpenClaw to reduce information gaps, the situation for subjective fund managers caught in the middle—watching research results produced with effort, yet being hit by quant reduction and pressured by retail investors—becomes quite awkward—facing AI FOMO and anxiety.

During the Spring Festival, I reviewed an annual report of a top subjective manager in Shenzhen. He lamented that fund managers have overly high expectations of researchers:

They hope researchers can stay sensitive to the market, promptly identify opportunities, provide leading research and judgments, and even stay constantly in the “core circle.” If a researcher can do all that, why need a fund manager? They can trade on their own and get rich, so why serve a fund manager?

So, he lowered expectations—researchers only need to focus on specific targets and issues, not on discovering opportunities or giving investment advice; those are the fund manager’s responsibilities.

Conversely, if a subjective fund manager only needs someone who doesn’t get involved in core industry circles and relies solely on desk analysis to track targets, then such a researcher might soon be replaced by an AI agent.

Epilogue

Living in the A-share market these past two years feels like being on an acceleration button.

Especially in the first half of this year, so many things happened. Last year’s Spring Festival saw DeepSeek release; during Qingming, the “Dunce King” imposed violent taxes; this Spring Festival, everyone was raising lobsters. Before the Lunar New Year even ended, the Middle East started fighting. Financial minds have been overloaded, unable to recall the last holiday without learning. At least for this editor, mental capacity is maxed out.

I remember two years ago, when communicating with fund managers about writing articles, they would happily describe their work as “dancing tap shoes to work.” But in the past two years, they talk about team “iterations,” investment philosophy “iterations,” and industry “iterations” without smiles.

AI develops so fast, industry progress is rapid—perhaps only through continuous iteration can one avoid being eliminated.

The industry remains too anxious.

AI doesn’t understand human nature; it can’t predict whether the current trades in the crowded A-share market are driven by third-order or fifth-order thinking; it can’t empathize—why someone has held two oil companies for so many years and still holds on, just waiting for the day to break even; it can’t take responsibility—if it loses 30%, it won’t be confronted by investors at the door, nor does it need to write apology letters or reflect on its soul.

If in the future AI replaces all fund managers and researchers, the Efficient Market Hypothesis would hold—no more Alpha, and perhaps no more Buffett-like figures.

So the real question is: in the future asset management industry, when AI takes over data scraping, model running, and report writing, what is left for humans? What remains is precisely the love for investing, intuition about uncertainty, and the reasons for staying despite being scolded that research is worse than AI.

We can’t change the trend of increasing AI participation, but we can change the internal fatigue and distraction caused by constant chasing and reacting.

Like in the game “Detroit: Become Human,” the ultimate choice for players isn’t to eliminate AI or submit to it, but to decide what roles humans and AI should each play.