FJU research reveals that legislator stock holdings do not consistently outperform the market; female legislators achieve better returns; political connections and media attention significantly impact stock prices.

Are Taiwanese legislators’ investment insights truly better than those of ordinary investors? A study conducted by the Department of Finance and International Business at Fu Jen Catholic University analyzed publicly disclosed legislator asset reports to establish a “legislator stock portfolio” and compared it with general market investments. The findings show that, under certain conditions, politicians’ stock holdings exhibit different investment characteristics, but overall performance is not consistently superior to the market.

The study tracked data from 2021 to 2023 and analyzed the relationship between legislator holdings, market attention, institutional investor behavior, and media exposure, aiming to answer a long-standing question: Do politicians have an informational advantage that leads to better investment performance?

Results indicate that legislator stock performance is not significantly better than that of non-legislators. However, the top 30% of legislators with the most re-elections achieved higher investment returns.

Congress also loves stock trading, with over half of legislators holding stocks

Using the 10th Legislative Yuan as a sample, the study found that out of 113 legislators, 61 held stocks in listed companies, accounting for approximately 53.98%.

By party affiliation:

- Democratic Progressive Party: 36

- Kuomintang: 22

- Other parties: 3

The remaining 52 legislators did not hold stocks.

Regionally, legislators from Taipei, New Taipei, Taoyuan, Taichung, Tainan, and Kaohsiung had notably higher stock ownership rates. The researchers speculate this may be related to urban areas with dense business activity and greater opportunities for politicians to engage with industries.

Legislator investment preferences: finance, plastics, and traditional industries

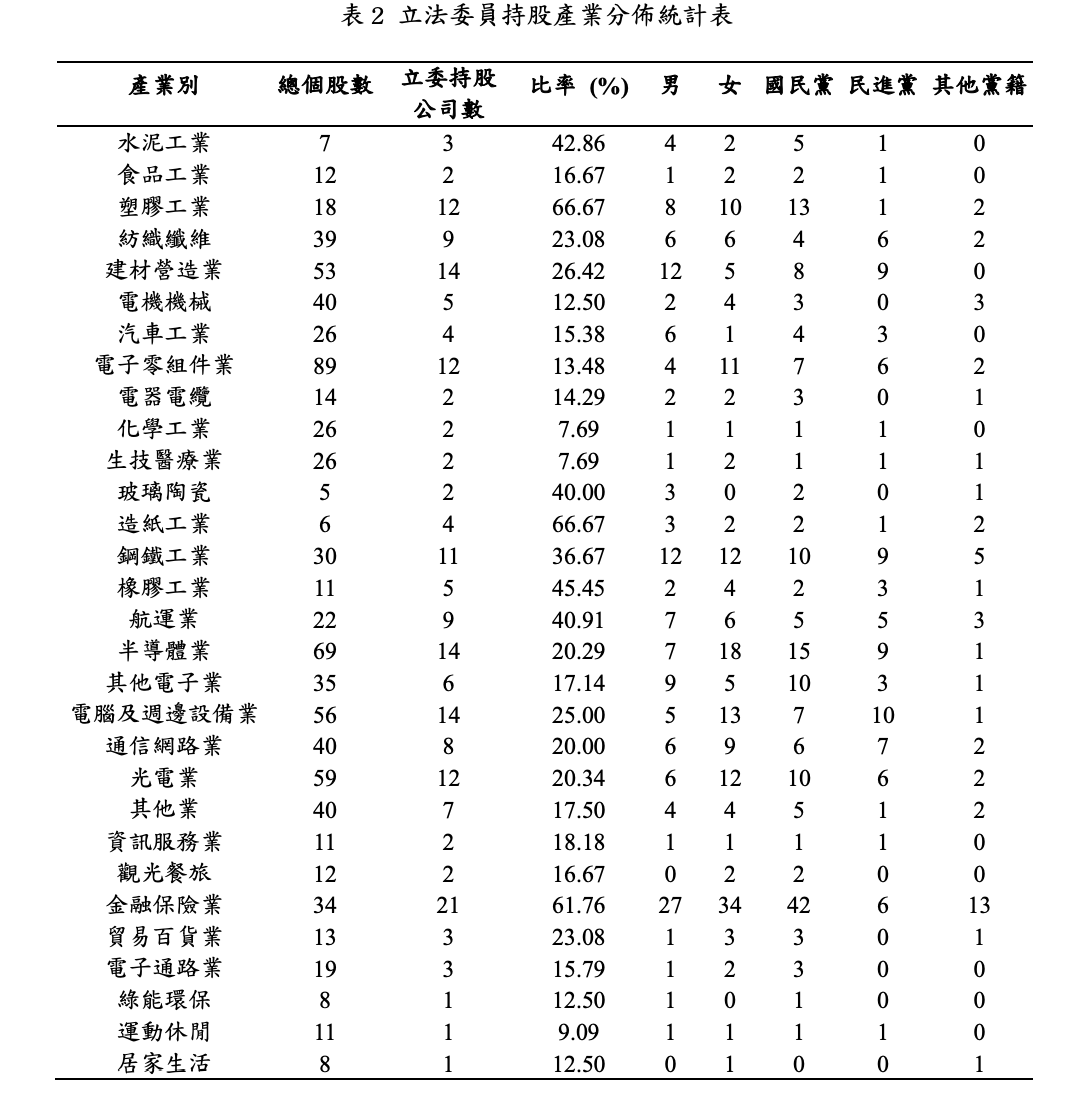

Image source: “Chain News” Industry Distribution of Legislator Stock Holdings, Source: Legislator Stock and Investment Portfolio Performance Program

The study compiled data on 191 listed companies held by legislators and analyzed their industry distribution. The results show a clear investment bias:

Primarily concentrated in:

- Financial and insurance sectors

- Plastics industry

- Paper manufacturing

- Steel

- Shipping

For example, in the financial and insurance sector, 61.76% of legislator-held companies are involved. Plastics and paper industries also exceed 66%. The study suggests that politicians prefer traditional industries with lower stock volatility and stable dividends over high-risk growth stocks.

Research shows: legislator holdings do not outperform the market long-term

The study developed two investment portfolio models:

- Equal-weighted portfolio (each stock has the same weight)

- Market-cap weighted portfolio (weights based on company market value, similar to ETFs)

Results indicate that in 2021, legislator portfolios outperformed the general market, with a 35.7% annual return compared to 28.7% for non-legislator holdings. In 2022, both portfolios suffered losses, and by 2023, the general market performed better. Overall, legislator holdings did not consistently outperform the market.

When using market-cap weighting, legislator portfolios showed significantly lower returns than the market.

Political donations and corporate directors’ political stances influence returns

Multiple studies suggest that links between corporations and political forces can impact stock prices and long-term financial performance. Academics generally agree that companies use political donations or directors’ political backgrounds to establish relationships with ruling parties, gaining advantages in policies, resources, or funding. Lin Yihong (2021) found that higher donations to elected parties correlate with higher cumulative abnormal returns, indicating political donations may significantly influence stock prices.

Additionally, Nianhang Xu, Xinzhong Xu, and Qingbo Yuan (2013) studied Chinese family businesses, finding that politically connected firms rely less on internal cash flow, suggesting political ties help access external funding. Wu, W., Wu, C., & Rui, O. M. (2012) found that political connections affect different types of firms differently: they may lower firm value and performance for local state-owned enterprises but can enhance value and operations for private companies.

Beyond political donations, the political stance of corporate directors may also influence market evaluations. Zhang Kaiwen (2010) reported that after the 2008 presidential election victory of the Kuomintang, companies with Blue camp directors showed positive abnormal returns, while Green camp directors’ companies showed negative abnormal returns.

Chen Liangyu (2014) found that when legislators or government officials hold corporate stocks, regardless of party, it impacts company value; after the Kuomintang’s 2012 victory, stocks invested in by Blue camp politicians showed higher abnormal returns, indicating that election outcomes can trigger market “win rallies.”

Women legislators’ investment performance is surprisingly better

The study also observed an interesting phenomenon: female legislators’ portfolios outperform those of male legislators on average. For example, in 2021, female legislators’ returns were 4.72% higher than males; in 2023, the gap widened to 6.73%. The researchers suggest this may be due to more conservative investment decisions and better risk management among women.

“Legislators’ stock focus” does not necessarily mean higher gains

The U.S. requires politicians to disclose stock holdings, leading to topics like Pelosi, the “female stock goddess.” The study also tested a common hypothesis: if multiple legislators hold the same stock, does it indicate a better investment?

The results show that companies held by multiple legislators are usually large corporations, but their short-term returns are not necessarily higher. These companies’ assets are, on average, about four times larger than those of companies held by individual legislators.

The researchers speculate that legislators tend to invest in large, stable, high-dividend companies. Following institutional investors yields better returns. Further analysis examined the overlap between legislator holdings and the “Big Three” institutional investors (foreign investors, trust funds, proprietary traders). The findings indicate that stocks with high proprietary trader holdings perform the best, followed by foreign investors and trust funds. The reason may be that proprietary traders have additional local information and market experience.

Media attention drives stock price increases

The study also used Google Trends search volume as a proxy for media attention. The results show that stocks in the top 30% by search frequency significantly outperform others. For example, in 2021, high-attention stocks returned 49.26%, while low-attention stocks returned 27.92%. The researchers believe that increased market attention attracts more investor capital, boosting stock prices.

- This article is reprinted with permission from “Chain News”

- Original title: “Are Taiwanese Legislators Really Better at Investing? Study Shows Top 30% of Re-Elected Legislators Earn the Most”

- Original author: Neo