a16z releases the March 2026 Top 100 Generative AI Consumer Apps list. ChatGPT weekly active users surpass 900 million and remain far ahead, but Claude and Gemini paid subscriptions are growing rapidly. AI is evolving from standalone products into foundational capabilities embedded in everything. This article is based on Olivia Moore (a16z)'s piece “Top 100 Gen AI Consumer Apps: March 2026,” edited and translated by Dongqu.

(Background: Is cryptocurrency no longer interesting? Builders are leaving en masse for AI, and intelligent systems companies may be the ultimate answer for the Web3 industry.)

(Additional context: OpenAI acquires AI safety firm Promptfoo: elevating safety testing and red team exercises to native Frontier features.)

Three years ago, we published the first edition of this list with a simple goal: to identify which generative AI products are truly used by mainstream consumers.

At that time, the boundary between AI-native (AI-first) companies and other software firms was very clear. Products like ChatGPT, Midjourney, and Character.AI were built from the ground up around foundational models. Meanwhile, other players in the software industry were still exploring how to utilize this technology.

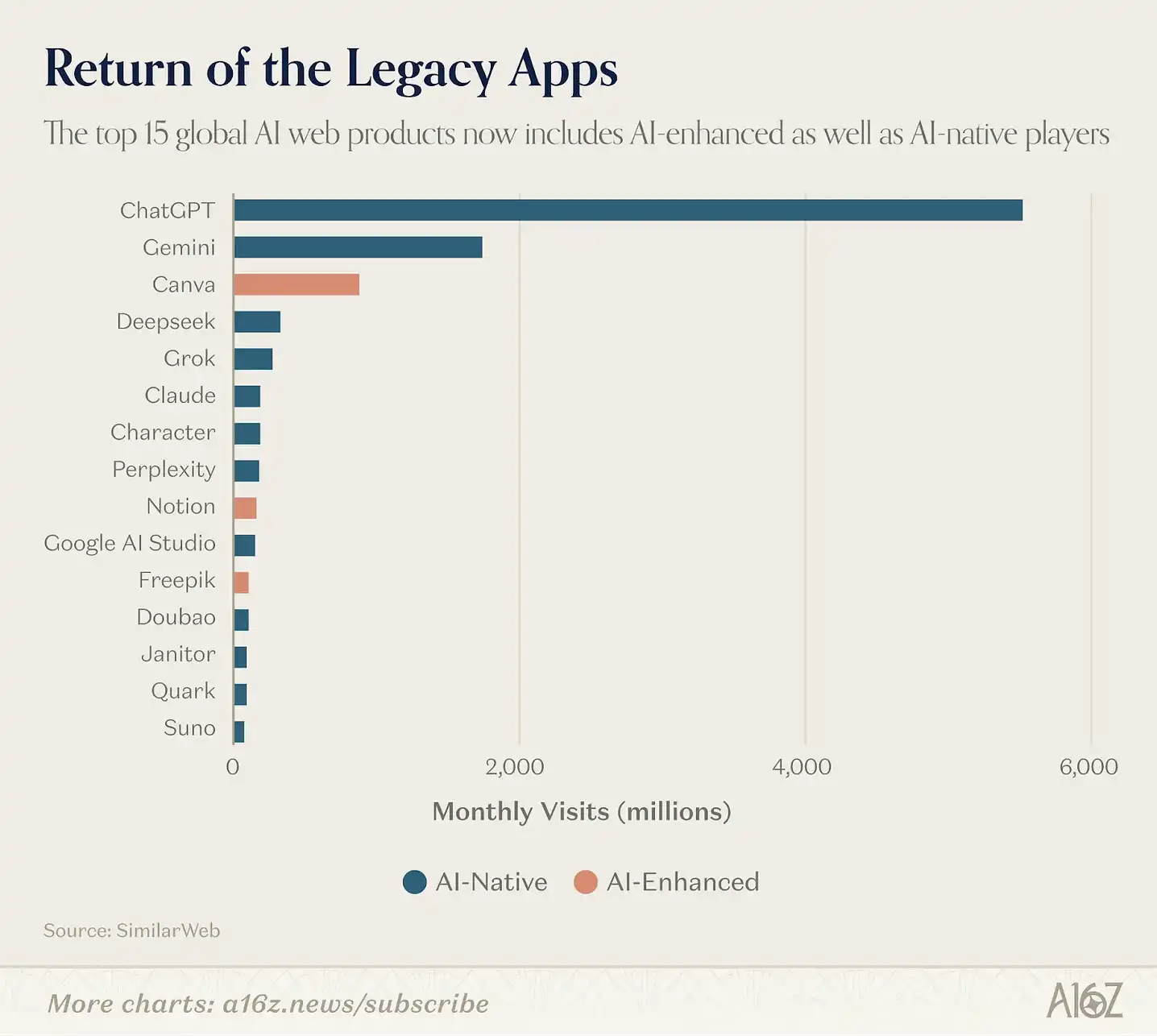

That distinction no longer holds. Take CapCut, a video editing app with 736 million monthly active users on mobile, whose most popular features heavily rely on AI—such as background removal, AI effects, auto subtitles, and text-to-video generation. Canva has built its entire growth engine on AI tools within its Magic Suite. Notion’s paid AI feature adoption rate soared from 20% to over 50% in a year, now contributing roughly half of the company’s annual recurring revenue (ARR).

Starting with this edition, we broadened our scope to include any consumer-facing application where generative AI has become a core part of the experience, including CapCut, Canva, Notion, Picsart, Freepik, and Grammarly. We believe this approach better reflects how people actually use AI, even though most top products remain AI-native.

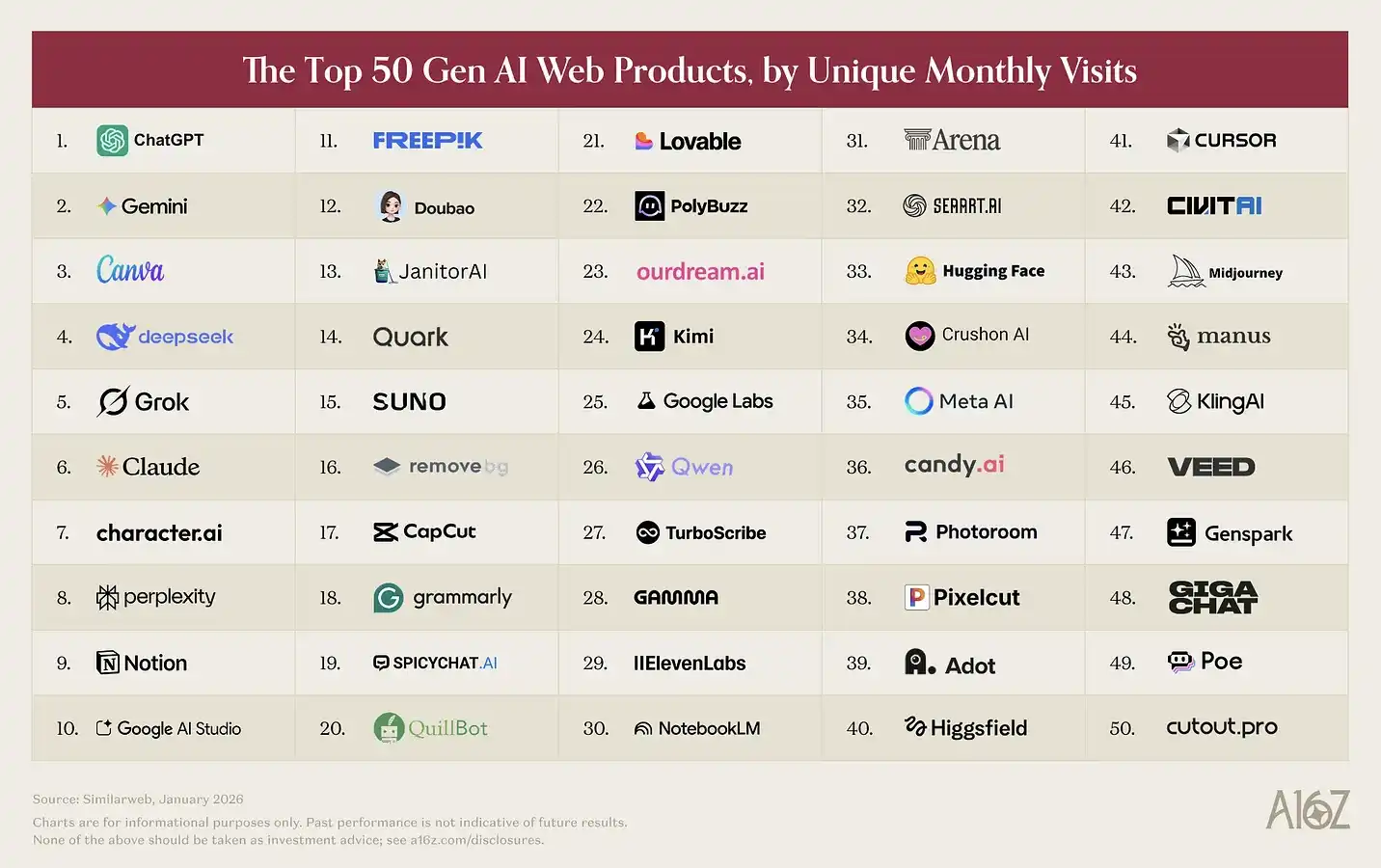

As usual, our web-based list ranks based on January 2026 SimilarWeb data for monthly unique visits; the mobile app list is based on January 2026 Sensor Tower data for monthly active users (MAU).

Here are some key observations:

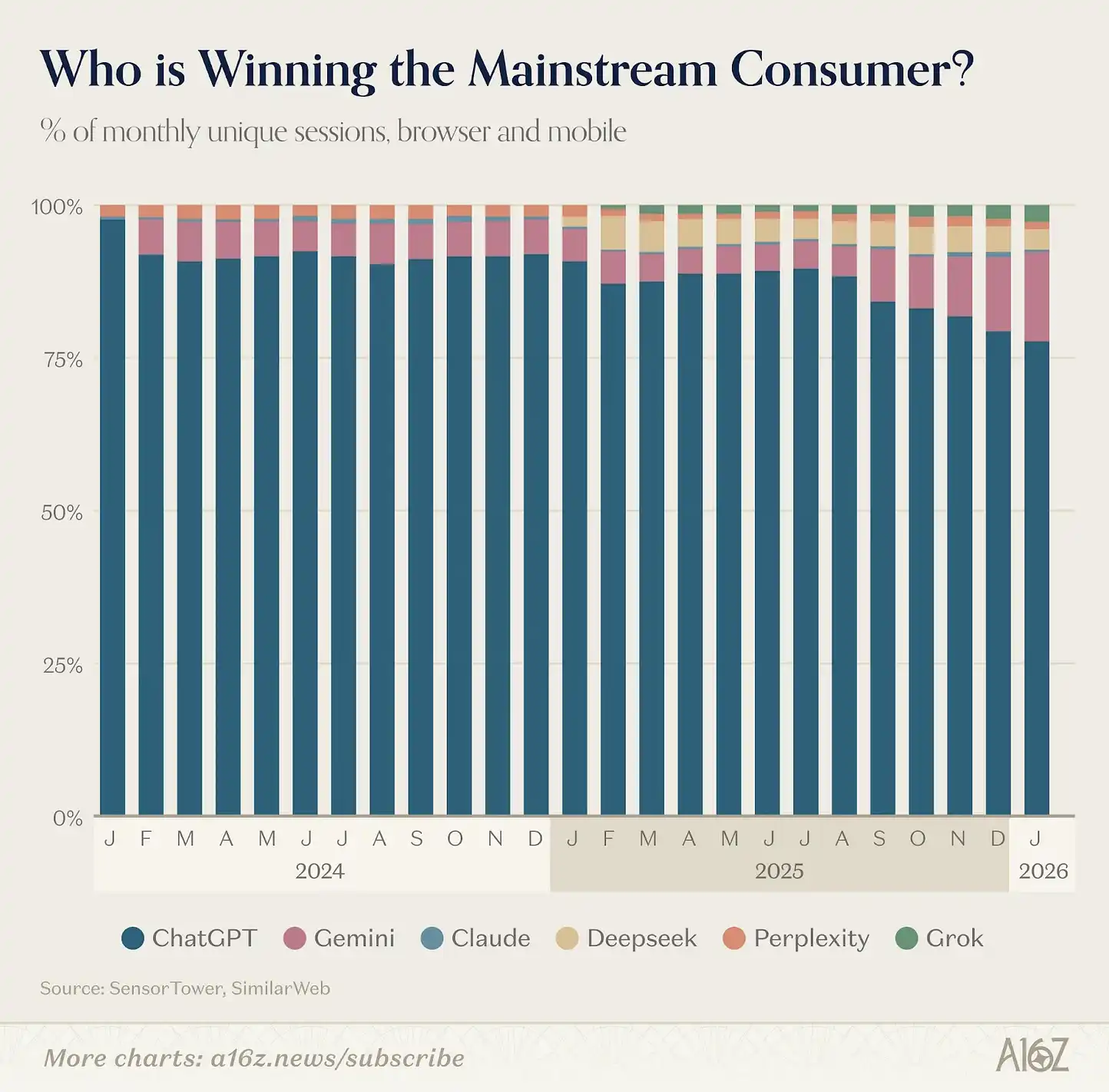

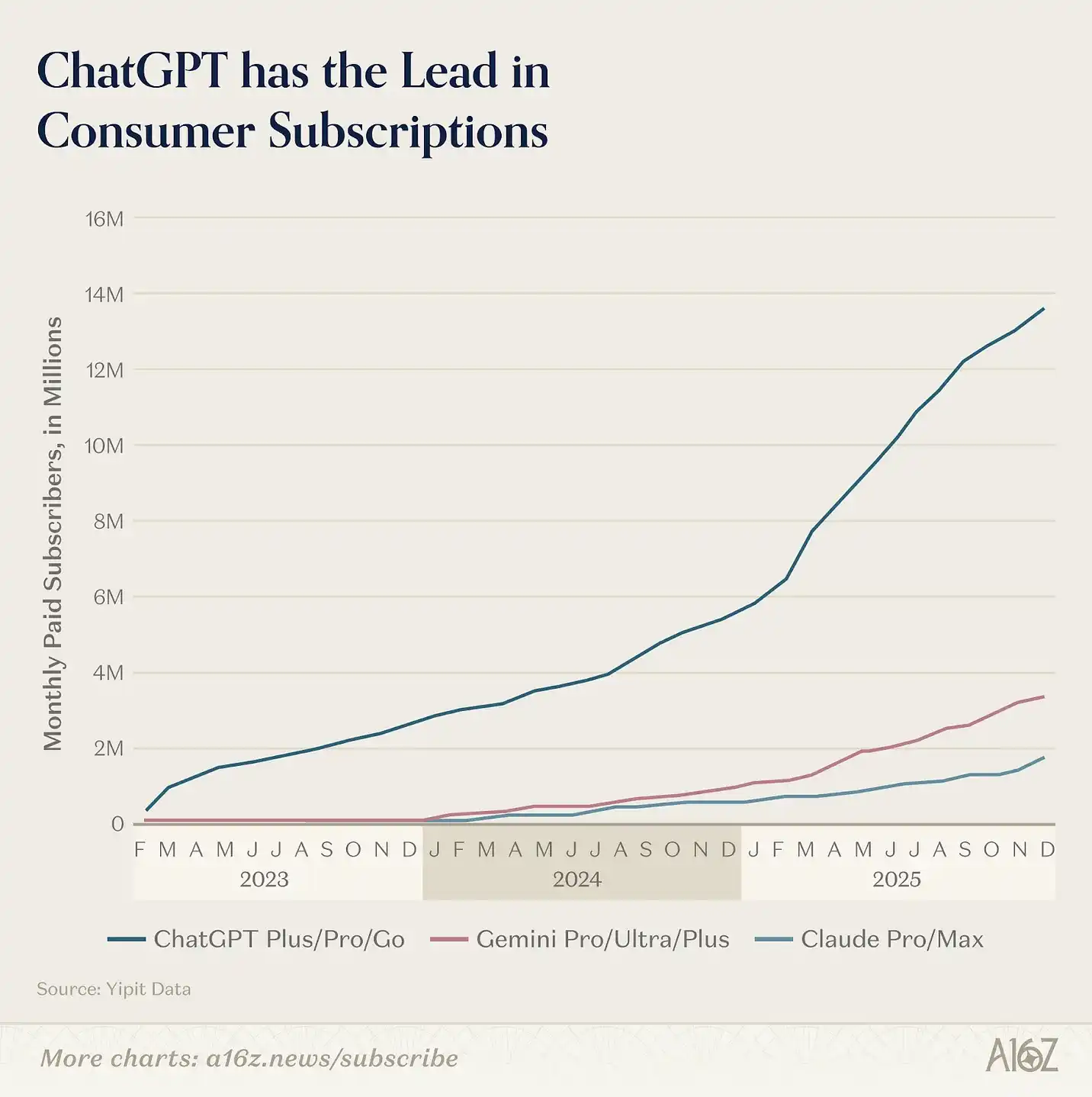

ChatGPT remains the dominant consumer AI product by scale. On the web, its monthly visits are 2.7 times that of the second-ranked Gemini; on mobile, its MAU is 2.5 times higher.

Over the past year, ChatGPT’s weekly active users increased by 500 million, reaching 900 million. Maintaining growth at such a massive scale is challenging, making this achievement especially remarkable. Currently, over 10% of the global population uses ChatGPT weekly.

However, we are also seeing the ecosystem expanding, with other horizontal platforms accelerating in specific use cases. Over the past year, paid subscriptions for Gemini and Claude in the U.S. have grown noticeably faster (though still much smaller than ChatGPT). In this metric, ChatGPT’s scale is about 8 times that of Claude and 4 times that of Gemini.

According to Yipit Data, as of January 2026, Claude’s paid subscription users grew over 200% year-over-year, while Gemini’s growth hit 258%. We also observe increasingly multi-platform usage: about 20% of ChatGPT web weekly active users also use Gemini within the same week.

What’s changing? Competitors are truly ramping up product launches.

Google has made significant breakthroughs in creative models. Nano Banana generated 200 million images in its first week, bringing 10 million new Gemini users; Veo 3 is widely regarded as a key breakthrough in AI video. Meanwhile, Anthropic continues to focus on prosumer markets, launching Cowork, Claude in Chrome, plugins for Excel and PowerPoint, and the highly anticipated Claude Code.

The importance of this competition lies not just in who is leading today, but in who can establish a structurally hard-to-replace position. In this space, “context continually accumulates advantages”: the more a large model understands your information and habits, the better it can serve you, encouraging more frequent use.

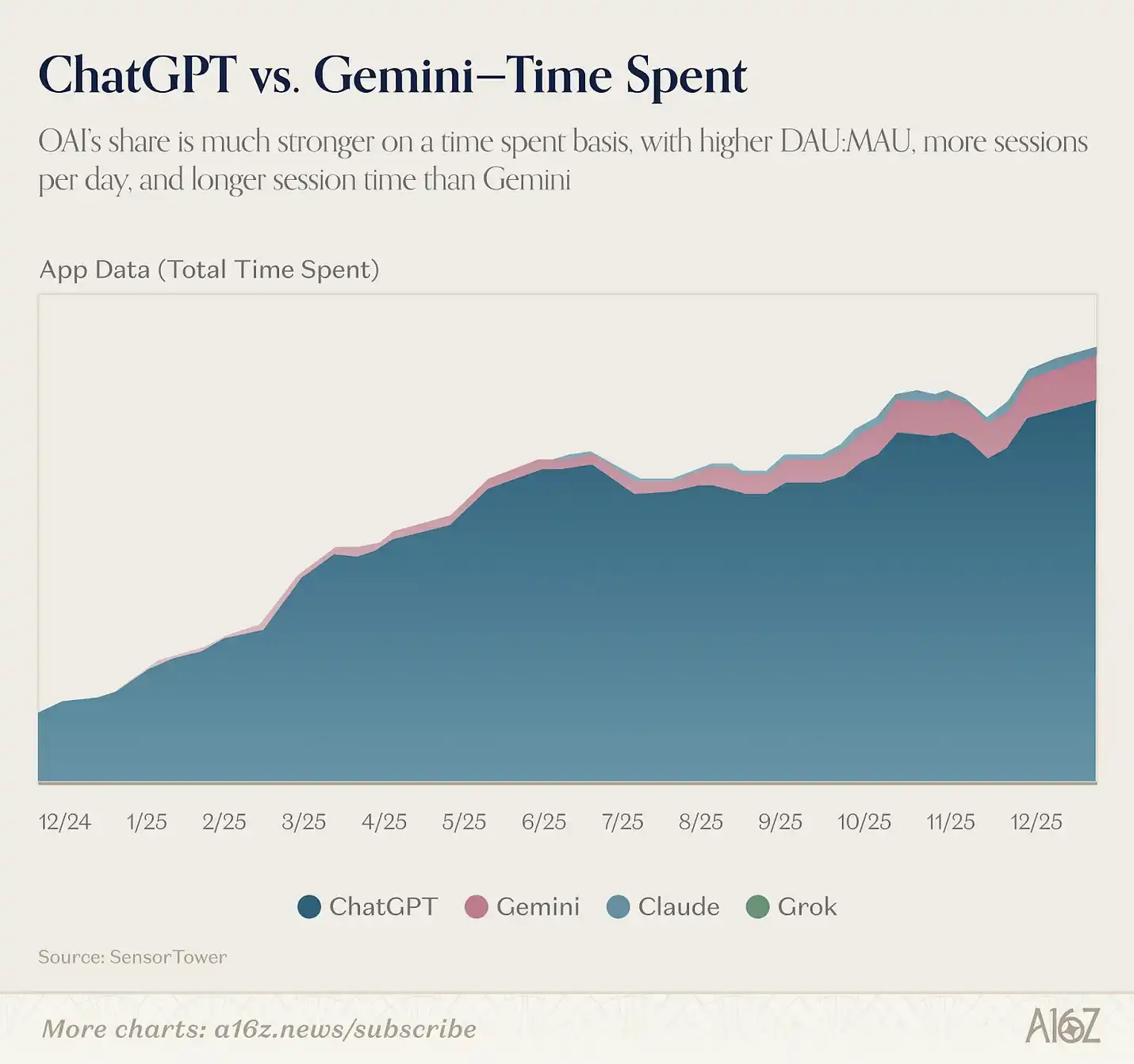

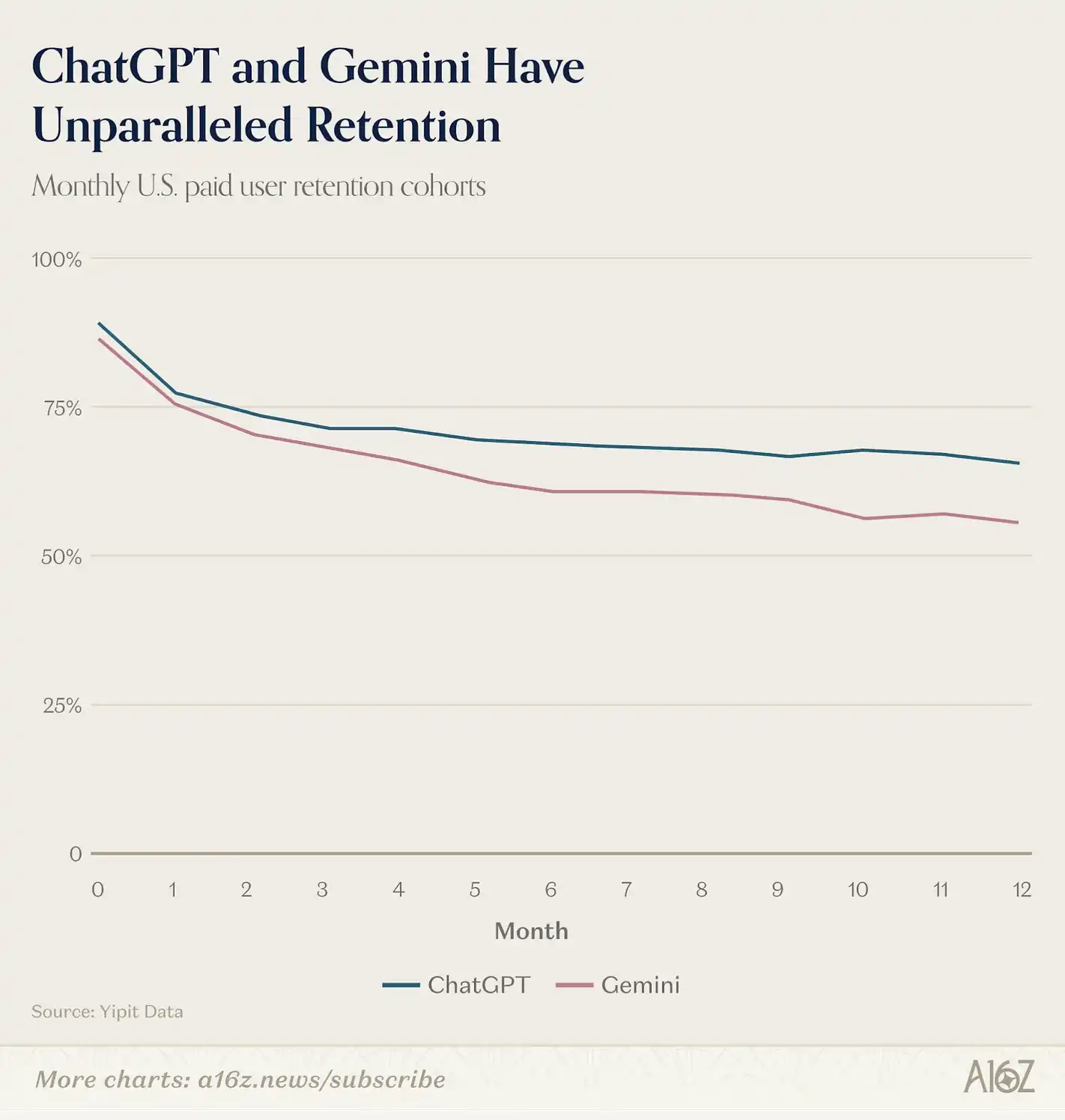

Preliminary data shows Gemini’s web user sessions per month are rising, but still about 1.3 times lower than ChatGPT; on mobile, ChatGPT’s advantage is even clearer, with 2.2 times more sessions per month. According to Yipit Data, both companies have industry-leading retention rates among paid consumer users in the U.S.

The next layer of “lock-in effect” comes from application ecosystems.

Both ChatGPT and Claude have launched connector ecosystems—ChatGPT’s GPTs and Apps, and Claude’s MCP integrations and Connectors—allowing users to build workflows on top of their assistants. Once users connect AI to their calendars, email, CRM, and other systems, switching platforms becomes significantly more costly. Meanwhile, developers tend to focus on the largest ecosystems, creating a flywheel effect similar to past platform wars.

We are beginning to see two distinct platform paths emerge. Sam Altman has stated that OpenAI’s goal is “bringing AI to billions who cannot afford subscriptions,” which is why they are introducing advertising; he also mentioned OpenAI will launch a “Sign in with ChatGPT” identity system, making ChatGPT the default gateway for consumer internet access. Their ambition is to make ChatGPT the starting point for all activities: shopping, reservations, browsing, health management, and daily life.

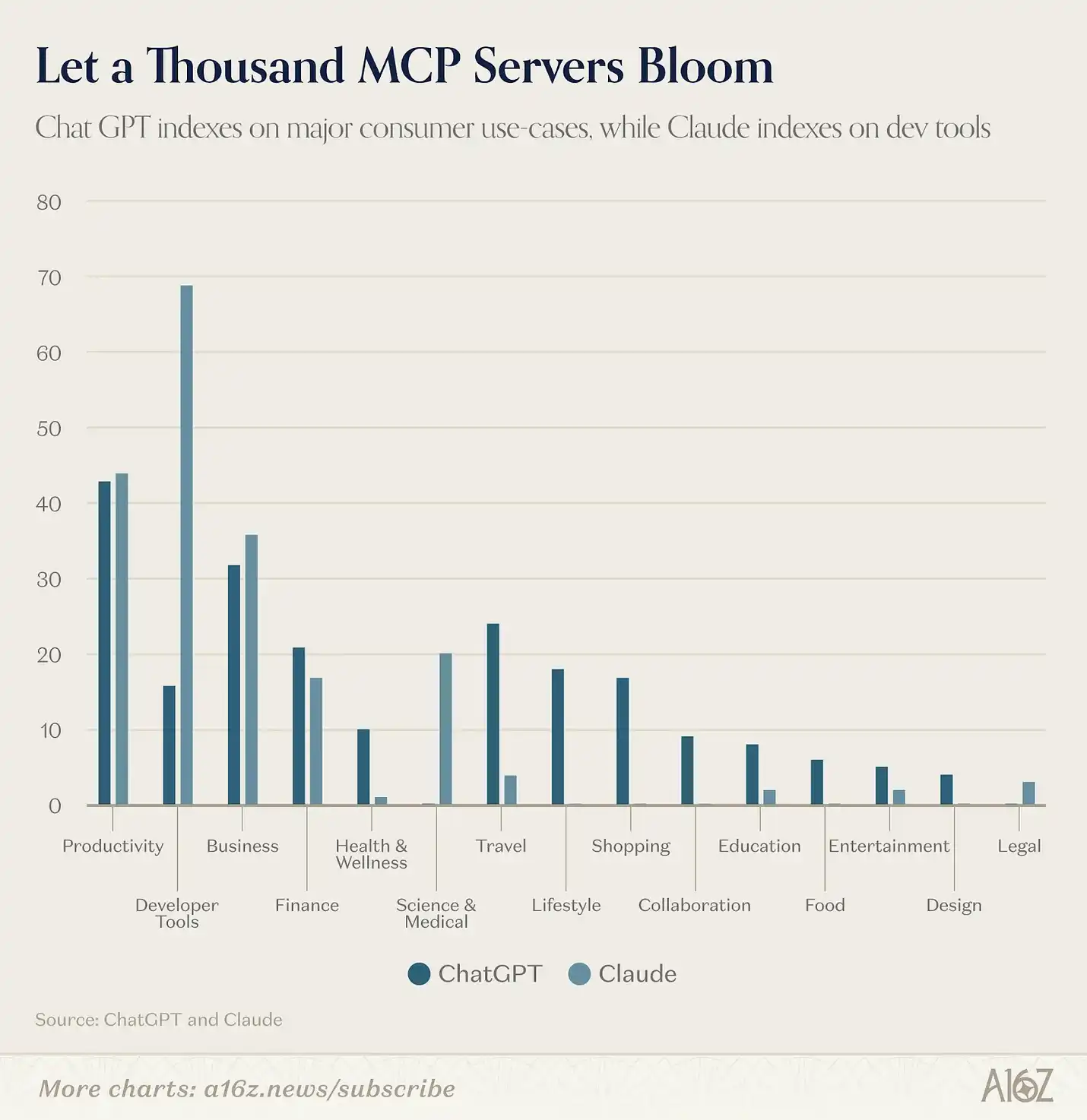

The app directories already reflect this direction. By the end of February, ChatGPT’s app store had 220 apps across 13 categories; Claude has about 160 official connector integrations and around 50 community-built MCP servers. Only 41 apps overlap, accounting for about 11% of both catalogs. Nearly all are general productivity tools: Slack, Notion, Figma, Gmail, Google Calendar, HubSpot, Stripe, etc.

Beyond these foundational tools, the paths of the two platforms are almost entirely separate.

ChatGPT has over 85 applications in categories like travel, shopping, food, health & fitness, lifestyle, and entertainment; Claude has little presence in these areas. These are consumer transaction scenarios: booking flights on Expedia, grocery shopping via Instacart, browsing listings on Zillow, tracking nutrition with MyFitnessPal. This is the most aggressive attempt by any AI company so far to become a consumer super-app.

In contrast, Claude’s exclusive integrations lean toward professional and enterprise scenarios: financial data terminals (PitchBook, FactSet, Moody’s, MSCI), developer infrastructure (Sentry, Supabase, Snowflake, Databricks), scientific and medical tools (PubMed, Clinical Trials, Benchling), and an expanding open-source MCP community. This ecosystem remains outside ChatGPT’s current scope.

Anthropic seems to focus on heavy AI users—developers, knowledge workers—who are more willing and able to pay for higher-cost direct subscriptions. While ChatGPT has also launched products targeting this group (e.g., Codex, Frontier), OpenAI explicitly aims to make ChatGPT a platform for mass users. As their user base grows, more monetization channels may open. They have begun testing advertising, and platform transaction revenue sharing (take rate) is a natural extension.

If AI assistants ultimately evolve from chat windows to operating environments, the outcome may not resemble the search wars dominated by a single player with 90% market share; instead, it could resemble the mobile OS battle: two very different platform philosophies, each building a trillion-dollar ecosystem.

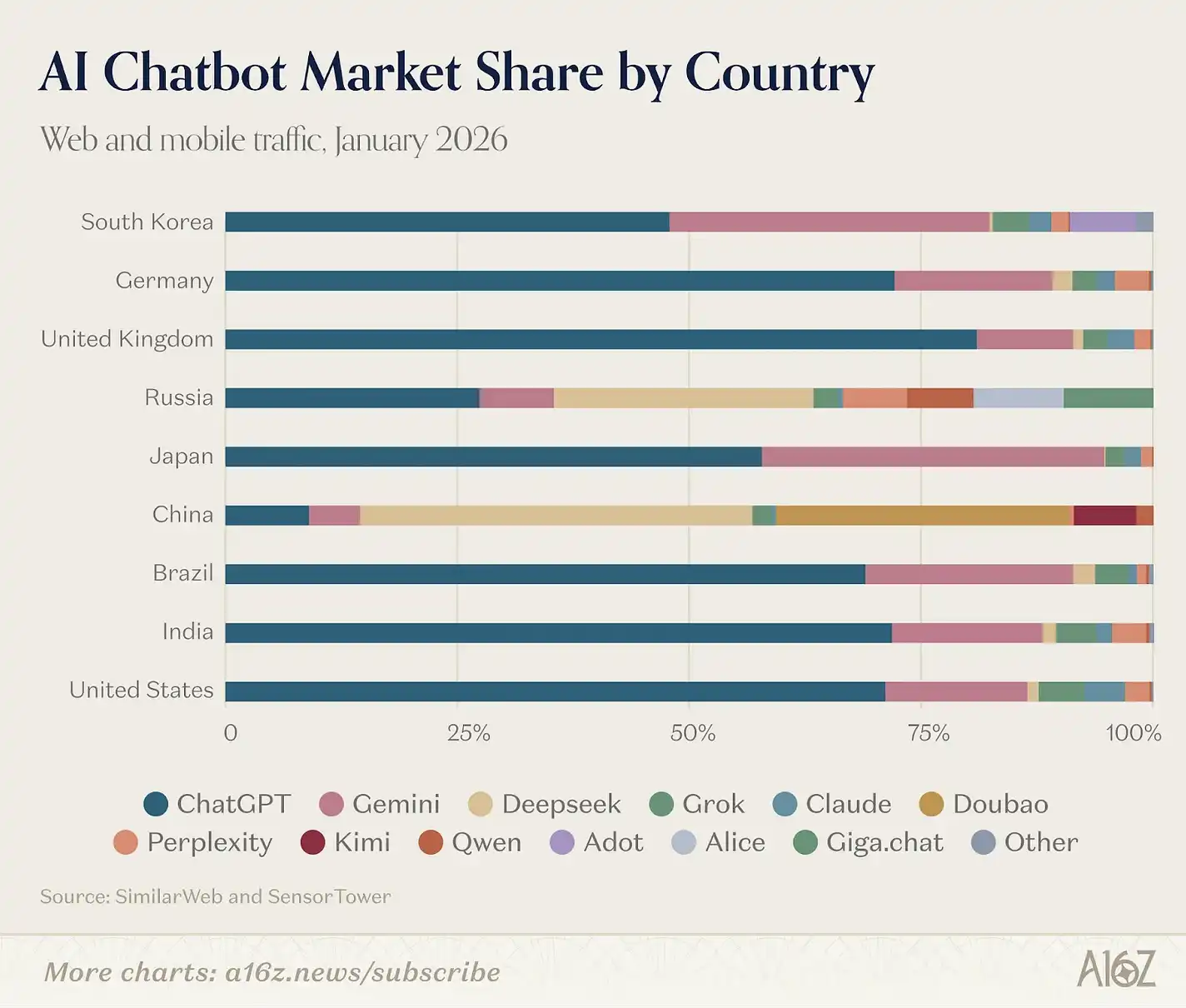

Geographically, the AI market is gradually splitting into three independent ecosystems, with widening gaps.

Western AI tool users are still highly similar. The main markets for ChatGPT, Claude, Gemini, and Perplexity are almost the same: the U.S., India, Brazil, the U.K., and Indonesia (in different order). In China and Russia, these products have little substantive usage, mainly due to policy factors—since 2022, Western sanctions have limited AI tool use in Russia; China requires AI providers to register, local data storage, and content censorship.

DeepSeek is currently the only product bridging these two camps. Its web traffic distribution is 33.5% China, 7.1% Russia, 6.6% U.S.; mobile distribution is similar. Meanwhile, Chinese users also heavily use ByteDance’s Doubao and local models like Kimi.

Russia, which previously had almost no independent market in our list, is now emerging as a third pole, with the second-highest DeepSeek penetration rate. Yandex Browser, integrated with Alice AI assistant, has reached 71 million MAU, making it one of the top ten mobile AI products globally. Sber’s GigaChat has also entered our web list for the first time. This pattern is similar to China’s development path—market gaps created by sanctions were quickly filled by local products within two years.

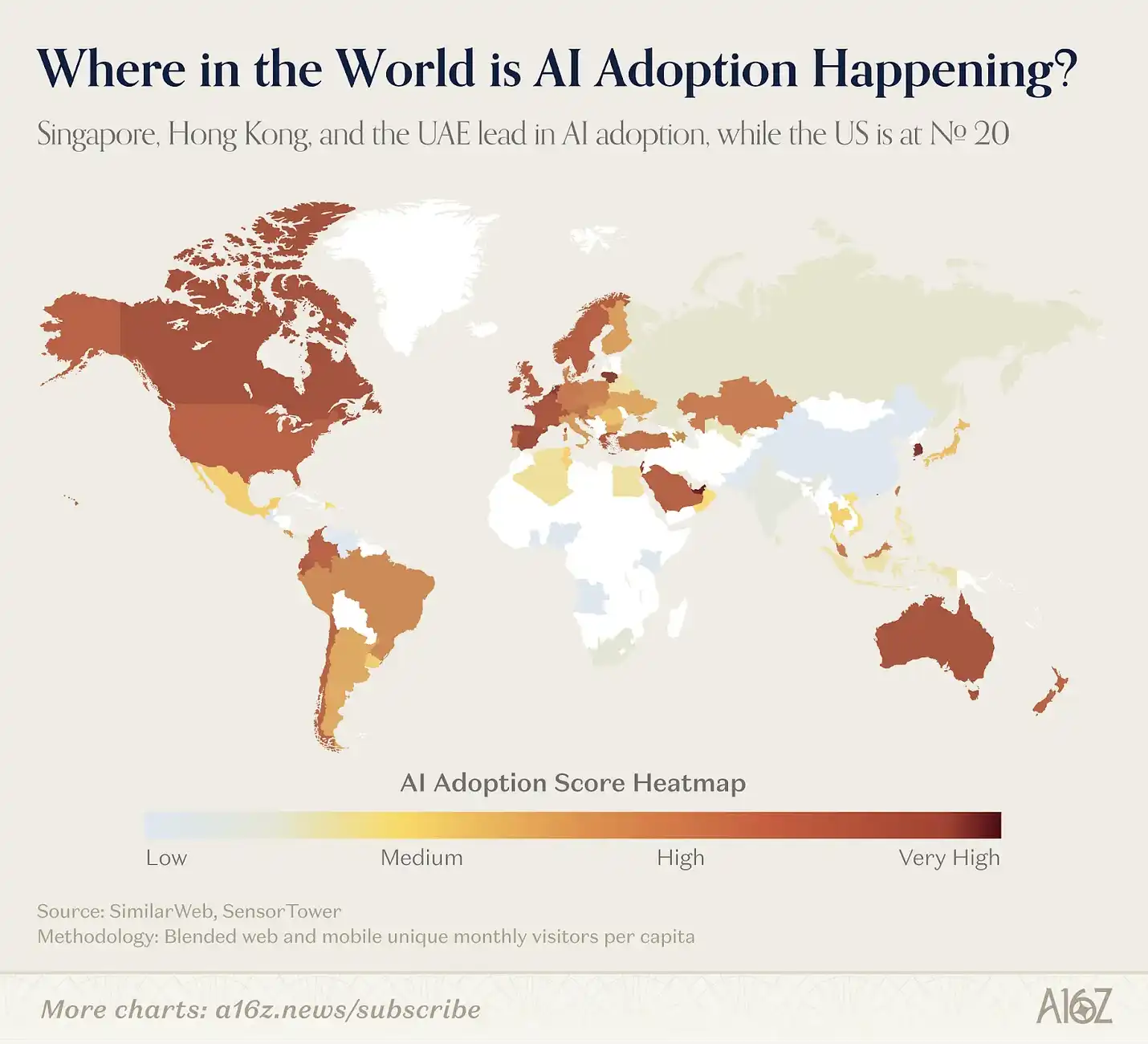

To assess AI adoption per capita, we built a simple index combining per capita web visits and per capita mobile MAU, scoring products from 0–100. The results reshape the global landscape: Singapore ranks first, followed by UAE, Hong Kong, and South Korea. The U.S., birthplace of most AI products, ranks 20th.

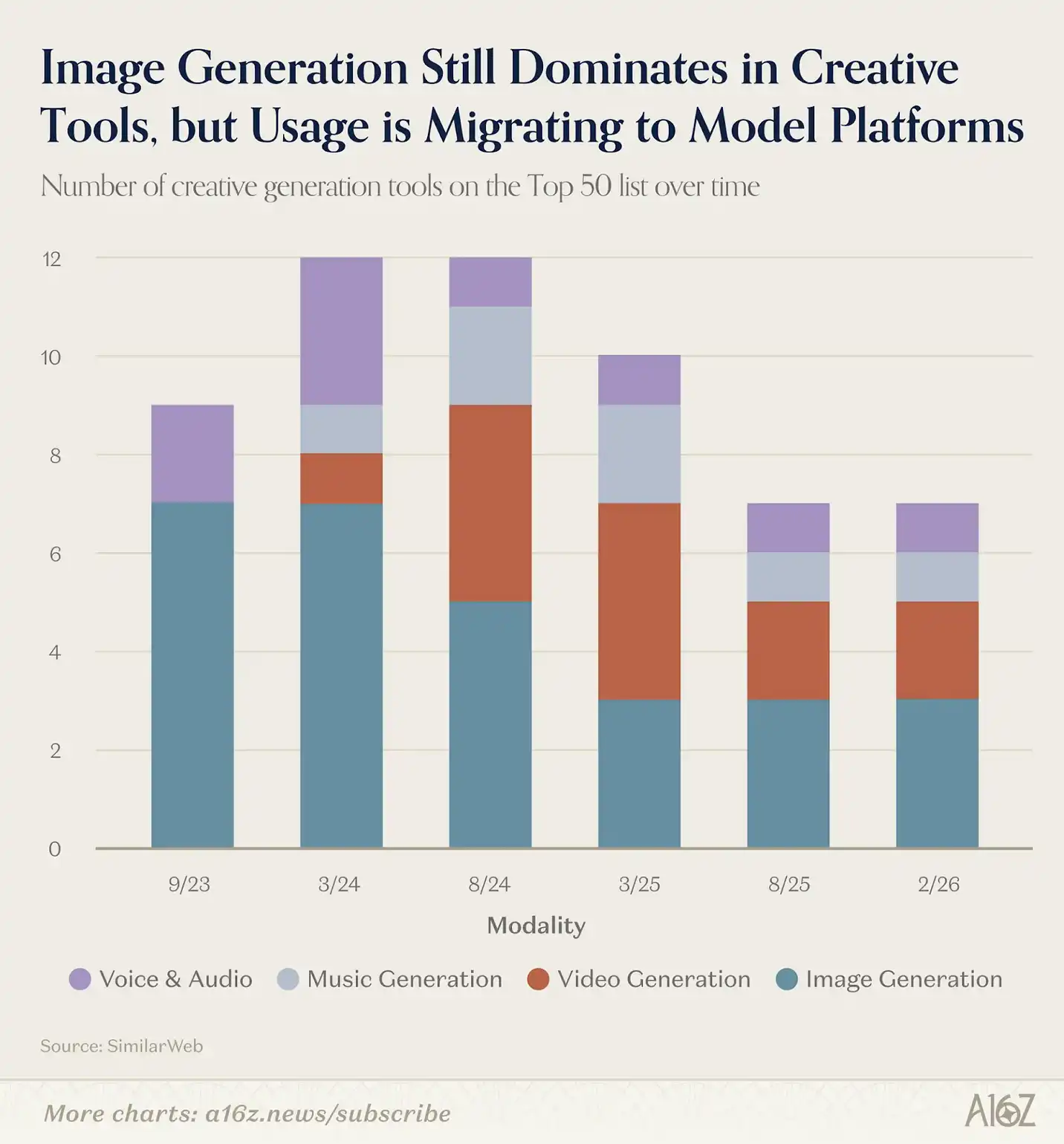

Midjourney, DALL-E, and Stable Diffusion were among the earliest products to introduce large numbers of early users to generative AI, all launched before ChatGPT. In the early days, image generation tools dominated creative applications (video and audio came later), and they held a clear advantage in our initial lists. But the landscape has evolved significantly.

In our September 2023 list, 7 of the top 9 web creative tools were image generators. Three years later, only 3 image generators remain, but the total number of creative tools is still 7. The shift is in filling new categories: video, music, and speech generation now replace image generation as the dominant segments.

The change in image generation is mainly due to “bundling.” As ChatGPT (GPT Image 1.5) and Gemini (Nano Banana) incorporate built-in image models, the barrier to entry for independent image generators has risen sharply. Our earliest list had Midjourney in the top 10; now it’s fallen to 46. The remaining products—Leonardo, Ideogram, CivitAI—serve niche creator communities with specialized features rather than competing directly with general-purpose generators.

The most notable change in this list is in video generation. Kling AI, Hailuo, and Pixverse have accumulated real user bases, with Chinese models leading in quality. If Seedance 2.0-based applications appear in the next list, we wouldn’t be surprised. Meanwhile, Veo 3 is the first U.S. model close to this quality level, significantly boosting Google Labs’ traffic, moving from 36th to 25th.

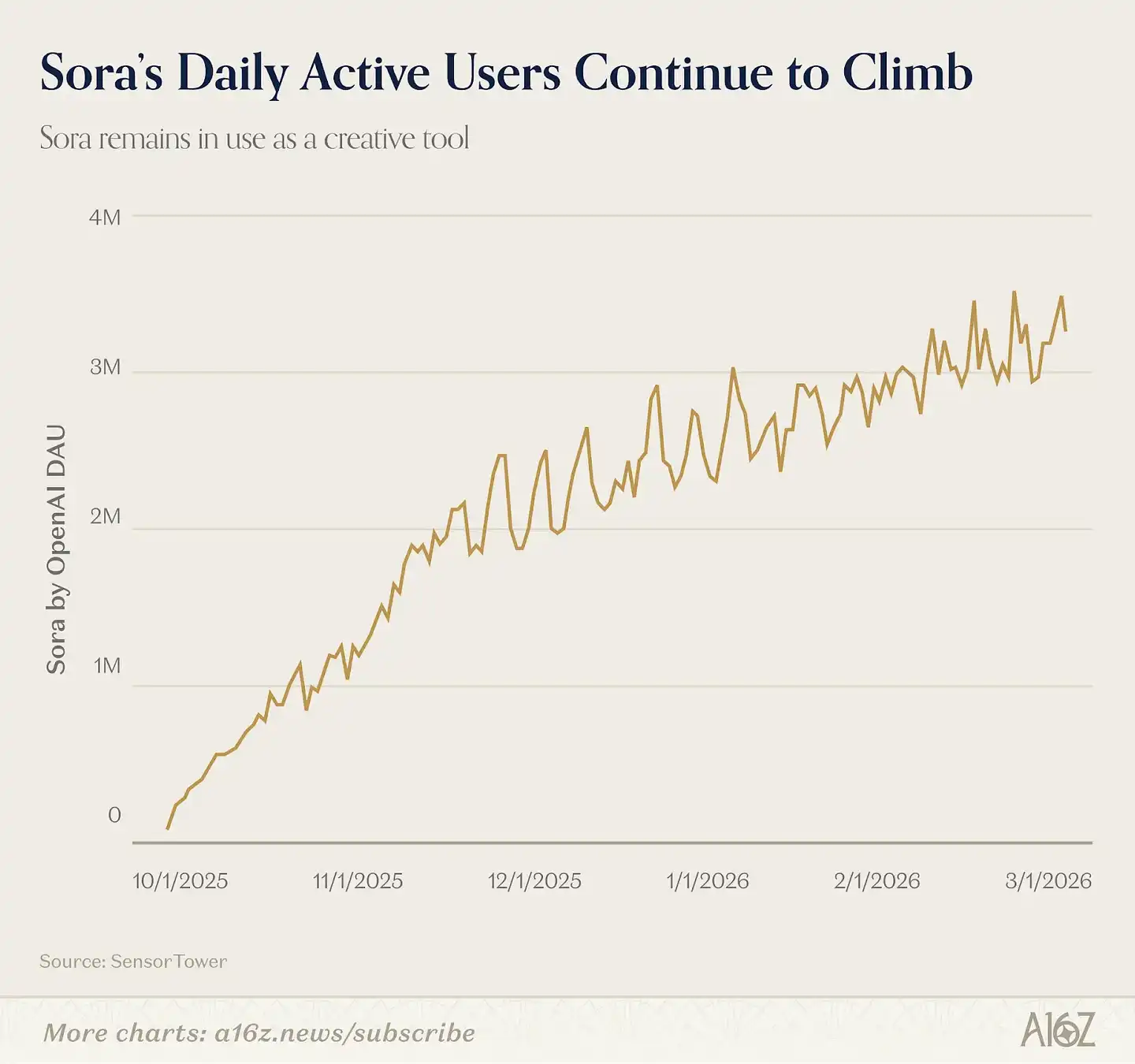

Who’s missing? Sora. OpenAI launched its flagship video model Sora 2.0 as a standalone app in September 2025, allowing users to upload their digital avatars (Cameo) and generate videos with real people. Sora topped the U.S. App Store for 20 days and hit 1 million downloads faster than ChatGPT. But downloads have since declined, as Sora did not develop into a viral social app (no one has cracked the “AI + social” combo yet), so it didn’t make this list. However, according to Sensor Tower, daily active users on mobile still exceed 3 million. Many AI video creators continue to use the model, though content is often posted elsewhere.

Music and speech domains are more stable.

Suno (ranked 15) maintained its position from the previous list; ElevenLabs has been on every list since September 2023. Its core capabilities—voice cloning, dubbing, audio production—remain highly specialized and are not simply “features” within large models.

The pattern here is: when giants like Google and OpenAI focus their creative capabilities on certain areas (e.g., images, increasingly videos), independent products’ traffic tends to shrink. But opportunities still exist to build more stylized, higher-monetization products for niche audiences. Conversely, in areas where giants have yet to fully enter (e.g., music and speech), market space remains larger.

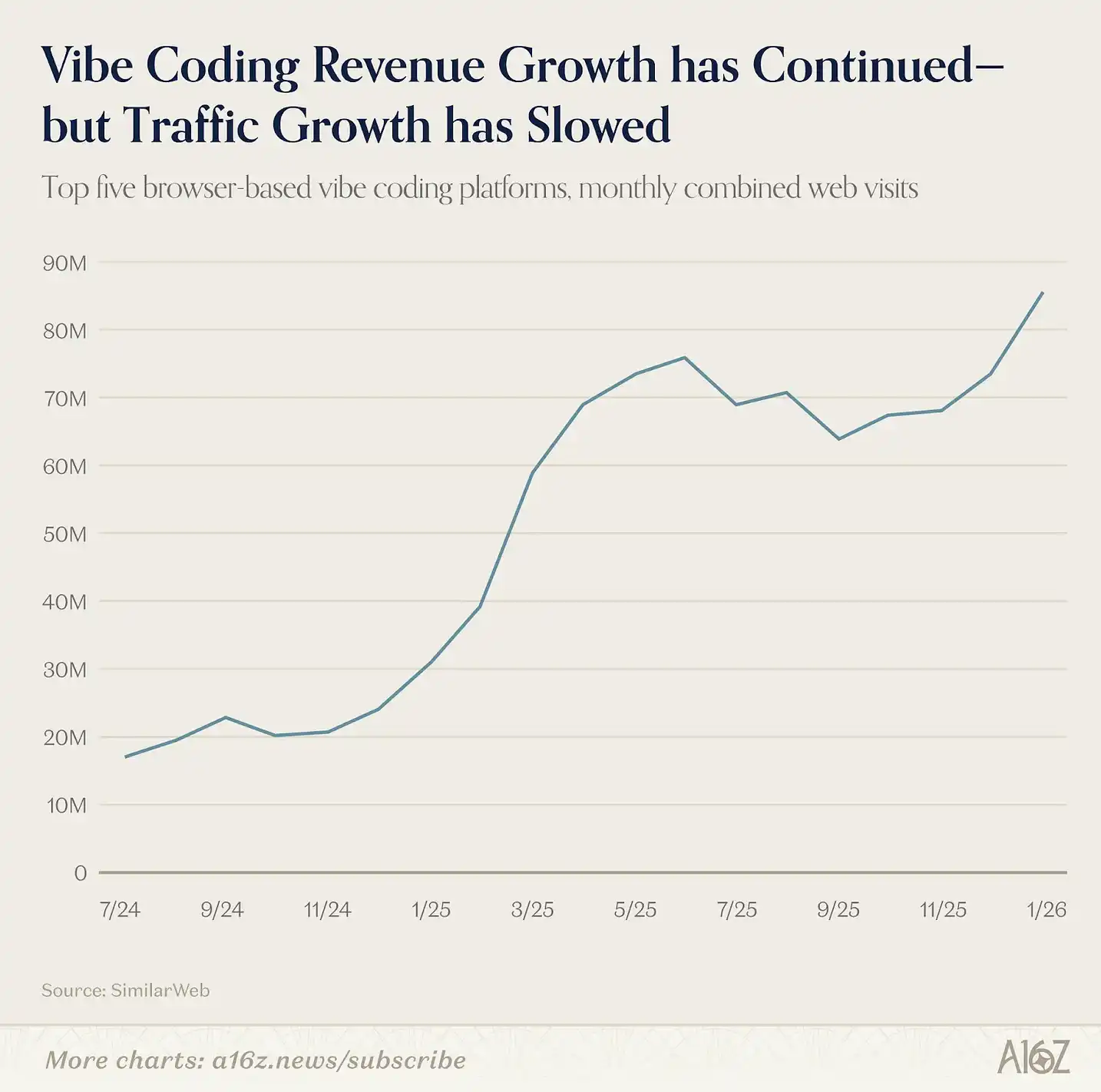

The shift toward Agentic AI didn’t start with this list but began earlier, with the emergence of “vibe coding” in the previous edition. When Lovable, Cursor, and Bolt entered our list in March 2025, they represented a new product form: AI no longer just answers questions or generates content but begins to “build things” on behalf of users. This is a form of agent behavior focused on specific verticals.

Evidence shows vibe coding has strong retention among technical (and semi-technical) users. Replit and Lovable remain on this list, and Claude Code (via Claude) also appears. There’s still room for growth, as this trend hasn’t yet reached the mass market. The top five vibe coding platforms continue to see increasing overall traffic, despite slowing from initial explosive growth—yet as developers and teams deepen their use, many products’ revenues continue to rise.

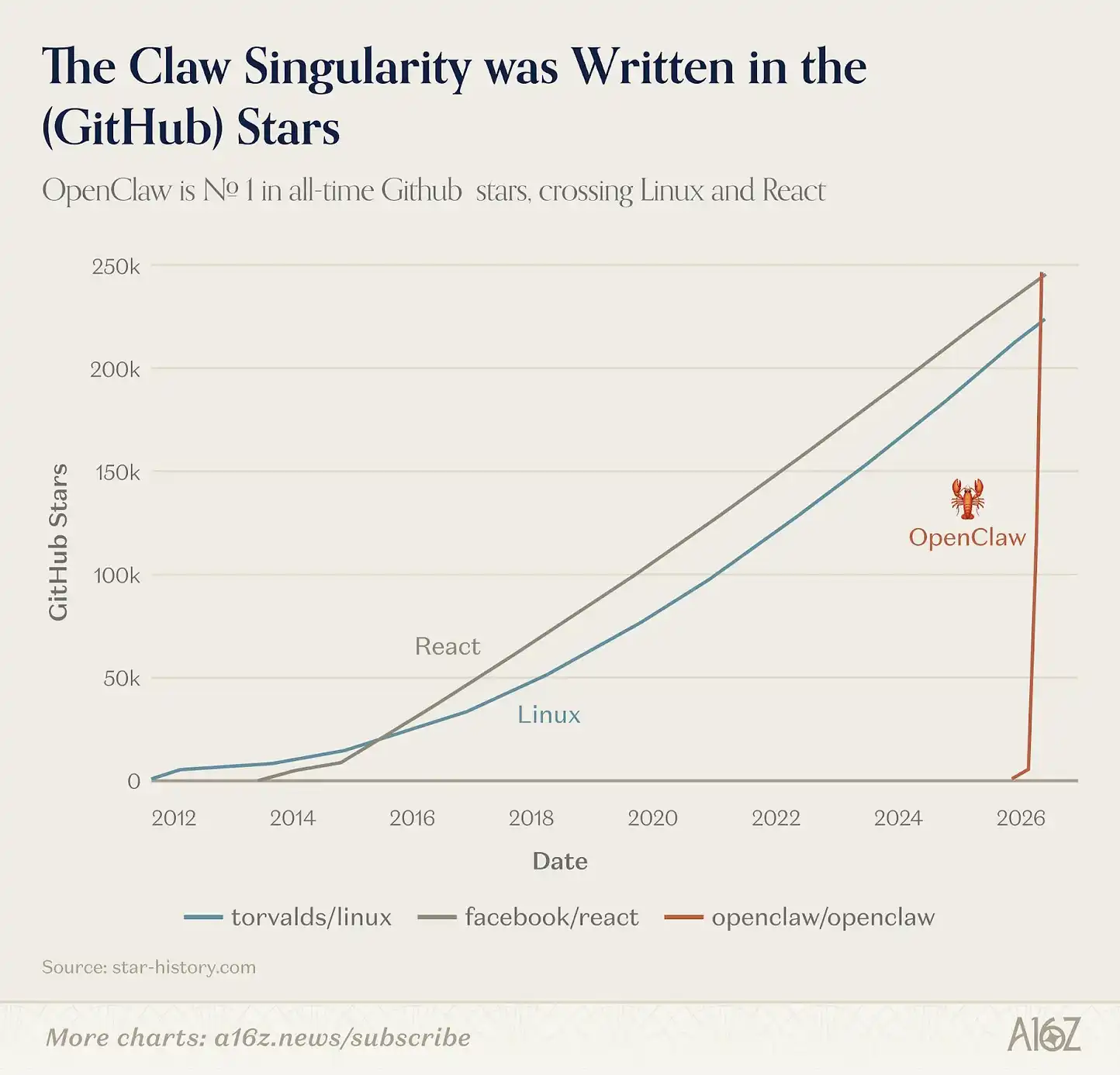

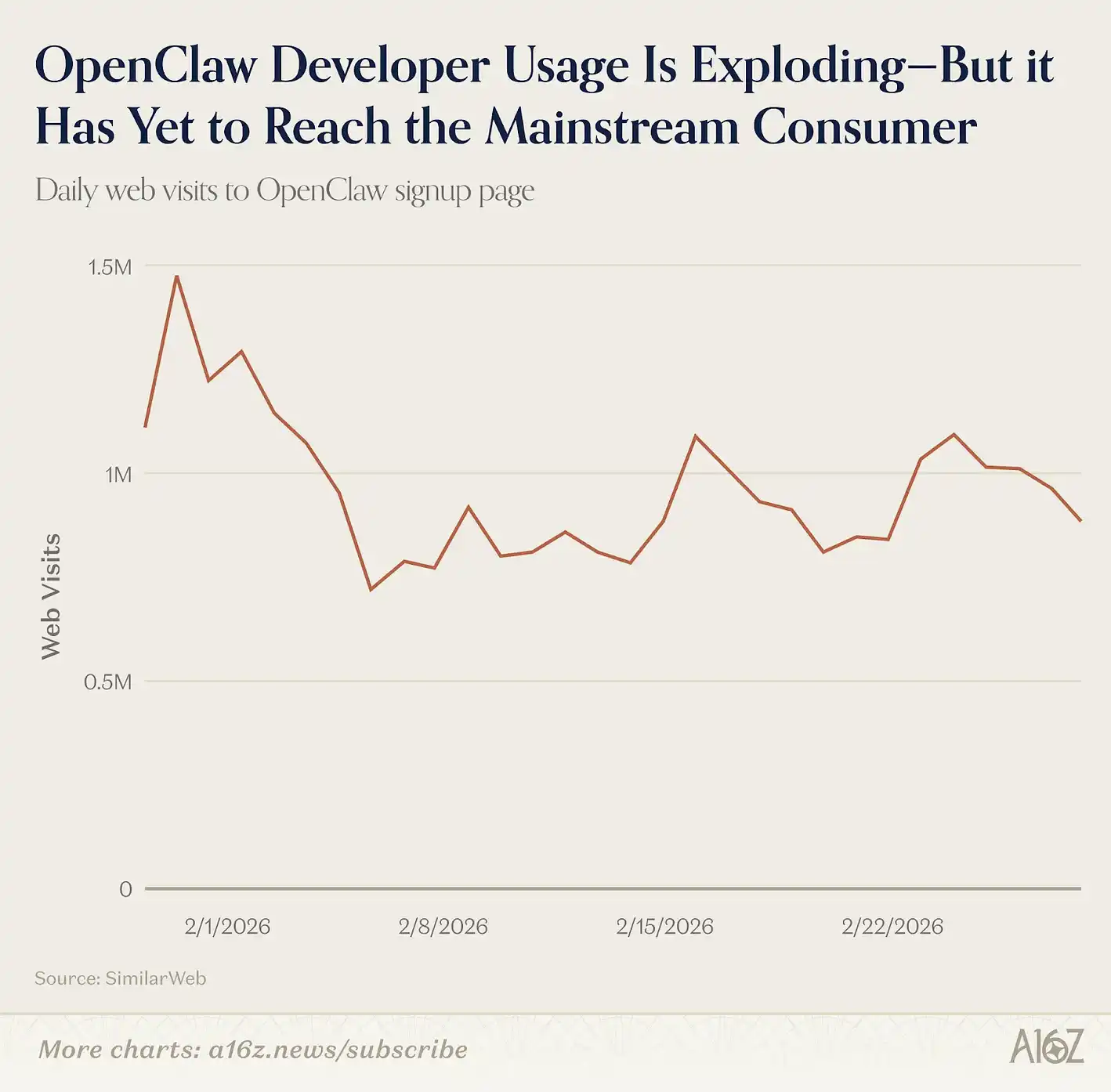

Recently, horizontal agents have also appeared. In January 2026, an open-source project called OpenClaw rapidly grew from a solo developer’s side project to 68,000 GitHub stars within weeks, gaining mainstream media attention. Created by Austrian developer Peter Steinberger, it’s a locally running AI agent that connects to messaging apps and performs multi-step tasks on behalf of users.

If ChatGPT was the moment consumers first realized AI could “converse,” then OpenClaw might be the moment they realize AI can “act.” It quickly gained popularity among developers; if our data extended to February, OpenClaw would likely rank in the top 30 web entries.

But OpenClaw isn’t yet a consumer product; installing and maintaining it requires some command-line knowledge. Still, interest among tech users continues to grow, and in early March, it became the most starred project on GitHub, surpassing React and Linux. Yet, based on new user traffic to its install site, it hasn’t yet entered the mainstream market; traffic remains relatively stable.

In February 2026, OpenAI acquired OpenClaw, suggesting a more user-friendly, consumer-oriented version may soon emerge.

OpenClaw isn’t the only horizontal agent on the list.

Manus and Genspark also made the rankings. These platforms enable users to delegate open-ended tasks (research, spreadsheet analysis, slide creation) to AI, which completes the entire workflow. This is Manus’s second appearance; since debuting, it was acquired by Meta in December 2025 for an estimated $2 billion. Genspark is appearing for the first time; it recently closed a $300 million Series B, with annualized revenue reaching $100 million.

On mobile, user interactions with agents often happen via messaging rather than dedicated apps. For example, users connect OpenClaw to WhatsApp, Telegram, or Signal during setup, then chat with it as if messaging a friend, while AI executes tasks in the background. Similar products like Poke even offer agent experiences via SMS.

These products will compete with the agent functions of general LLM assistants like ChatGPT, Claude, and Gemini. As these platforms build their own networks through Connectors and ecosystems, a key question is: will users adopt one product as their “main agent”?

The answer may become clearer in the next six months.

Previous editions of the list used two metrics: web visits and mobile MAU. Now, a new class of AI products is emerging that these metrics can’t fully capture. Over the past year, some of the most significant consumer AI growth has occurred in products that aren’t reflected in web traffic or mobile MAU.

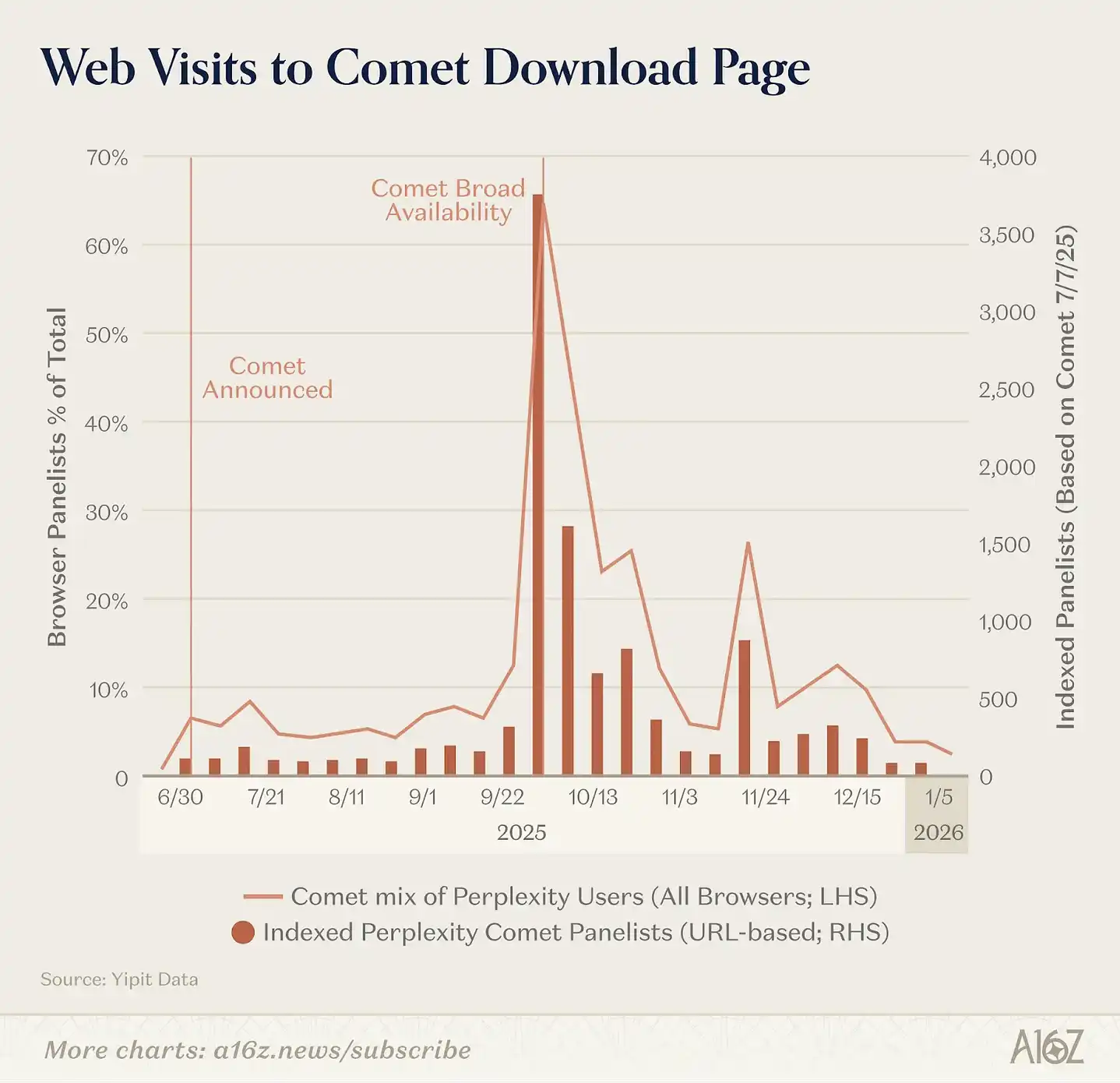

The most obvious change: browsers themselves are becoming AI products. Over the past nine months, OpenAI launched Atlas (a browser with ChatGPT built-in), Perplexity released Comet, and Browser Company (later acquired by Atlassian) launched Dia. According to Yipit, among these, Comet has had the biggest impact based on page visits, but no AI browser has shown sustained acceleration yet.

Meanwhile, some AI giants are integrating AI features into existing browsers rather than launching standalone AI browsers. Google integrated Gemini into Chrome and released Disco (beta), which dynamically generates web apps based on current tabs. Anthropic launched Claude in Chrome, connecting to user sessions of Claude or Claude Code, enabling real-world actions within the web environment.

Native desktop AI tools are growing even faster, especially among developers.

For example, Claude Code, a command-line AI agent for developers, reached $1 billion ARR in just six months. OpenAI also launched a Mac standalone Codex app; as of early March, it had 2 million weekly active users and continues to grow at 25% weekly. Meanwhile, Cursor remains in our top 50 web list.

For ordinary consumers, the most common standalone AI desktop apps are voice-related tools.

Products like Fireflies, Fathom, Otter, TL;DV, and Granola, mainly via product-led growth (PLG), are penetrating enterprise markets. These top five have combined monthly visits of about 20 million. At the same time, workspace apps like Notion (first time on the list) are increasingly integrating AI features—meeting notes, research agents, task automation, etc.

Finally, AI is embedding more and more into existing software people already use.

Anthropic launched Claude in Excel and PowerPoint; OpenAI released ChatGPT for Excel; Google further integrated Gemini into Workspace—Docs, Sheets, Gmail, and Meet now have native AI features. In January 2026, Google introduced Personal Intelligence, linking Gemini with Gmail, Photos, YouTube, and Search, enabling the assistant to automatically reference your hotel bookings, shopping history, photo library, and viewing habits without extra input.

This trend means our rankings are increasingly underestimating the AI products people use most daily.

A developer using Claude Code 8 hours a day or knowledge workers composing all emails via Wispr voice tools are heavy AI users but rarely reflected in web traffic data. As AI shifts from destination products (users opening a product to use AI) to a foundational feature, our metrics must evolve accordingly.