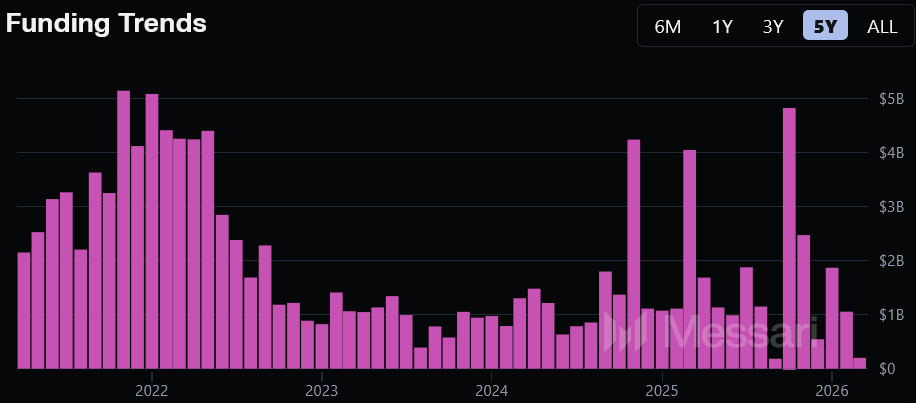

According to the crypto financing overview released by Messari on Sunday, from March 2025 to March 2026, crypto financing amounts increased by nearly 50% compared to the previous 12 months, but the number of completed transactions decreased by 46%. The average transaction size rose to $34 million, a 272% annual increase. Venture capital firms are focusing on later-stage and strategic large funding rounds rather than broad participation in early-stage projects.

Structural Shift in Financing Growth: Capital Concentration Replaces Broad Participation

(Source: Messari)

Messari’s data presents a market picture of “total growth but declining participation”:

Total Financing: Nearly 50% annual increase, significant expansion in capital size

Number of Transactions: Down 46% year-over-year, overall market activity contracts

Average Transaction Size: Increased to $34 million, up 272% annually, with a substantial rise in top-tier deals

Number of Active Investors: Down 34.5%, to 3,225, indicating a shrinking market participant base

Eric Turner pointed out, “Capital concentration is heavily skewed toward later-stage and strategic large funding rounds,” illustrating this with February data: the total crypto financing in that month was $795 million, with 44% concentrated in three deals, clearly showing a concentration effect.

February’s Top Three Financing Deals: Structural Dominance of Large Rounds

These three deals exemplify the current structural features of the crypto financing market—large, late-stage, strategic:

Tether invested $200 million in the online marketplace Whop, the largest single deal of the month, indicating that crypto-native institutions, represented by stablecoin giants, are strategically extending into traditional tech sectors.

Sports prediction market Novig raised $75 million in a Series B funding round led by Pantera Capital, a representative case of institutional capital recognition in the prediction industry.

ARQ, a Latin American fintech focused on stablecoins, completed a $70 million Series B funding round led by Sequoia Capital, demonstrating top-tier Silicon Valley VCs’ continued focus on crypto fintech in emerging markets.

Notably, the $795 million figure for February decreased by 65.3% compared to the previous 30 days, indicating high monthly volatility, with data heavily influenced by top deals.

Industry Funding Gap: Stagnation of Large VC Funding and AI Diversion Effects

Eric Turner also highlighted a structural issue worth noting: aside from Dragonfly Capital, no other major crypto venture firms have completed new funding rounds recently. He directly stated, “This industry needs some new capital.” This suggests that while the market’s capital stock is growing, the primary market’s new capital pool has relatively stagnated, raising concerns about long-term sustainability.

Meanwhile, some investment firms are shifting funds toward artificial intelligence and high-performance computing (HPC), leading to capital competition from adjacent sectors. Messari data shows that over the past three months, the most active crypto investors were Coinbase Ventures, QUBIC Labs, and Somnia.

In early-stage funding, Messari notes that the number remains relatively high but “quite dispersed,” such as Interstate raising $1.5 million from over 15 participants—including Bloccelerate VC and angel investor Sergey Gorbunov—indicating broad but relatively small early-market activity.

Frequently Asked Questions

What is the main driver behind the 50% growth in crypto financing over the past 12 months?

According to Messari data, the core driver is the expansion of late-stage and strategic large funding rounds, with the average deal size increasing to $34 million (up 272% annually). Capital concentration effects mean that even with a 46% decrease in transaction count, total financing still grew by about 50% annually.

How does current crypto financing compare to the peak periods of 2021-2022?

November 2021 and May 2022 marked historic peaks, with monthly financing reaching $4 billion. Since then, this milestone has only been achieved three times. While there has been annual growth in the past 12 months, the overall scale remains far below the levels of 2021-2022.

What impact does the stagnation of large crypto VC funding have on the industry?

Eric Turner pointed out that aside from Dragonfly Capital, no other major crypto VC firms have completed new funding rounds recently. The stagnation of primary market capital pools could pressure long-term investment funding, and Turner directly stated that “the industry needs some new capital.”

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.