MicroStrategy Faces a Major Confidence Test: Nasdaq Delisting Risk, Buyback Motives, and Executive Sell-Offs

Crypto markets are unsettled, with Bitcoin’s weakness dragging down the entire sector, accelerating bubble deflation and putting investors on high alert. As a leading Digital Asset Treasury (DAT) firm, MicroStrategy now faces mounting pressures: a sharp contraction in mNAV premiums, slower Bitcoin accumulation, executive stock sales, and the threat of index exclusion—all severely testing market confidence.

MicroStrategy Faces Crisis of Confidence, Potential Index Exclusion

The DAT sector is experiencing its darkest hour. As Bitcoin prices continue to fall, market premiums for major DAT firms have plunged, stock prices remain under pressure, the rate of Bitcoin purchases has declined or even stalled, and the business model is facing significant challenges. MicroStrategy has not escaped this turmoil, and now finds itself in a crisis of confidence.

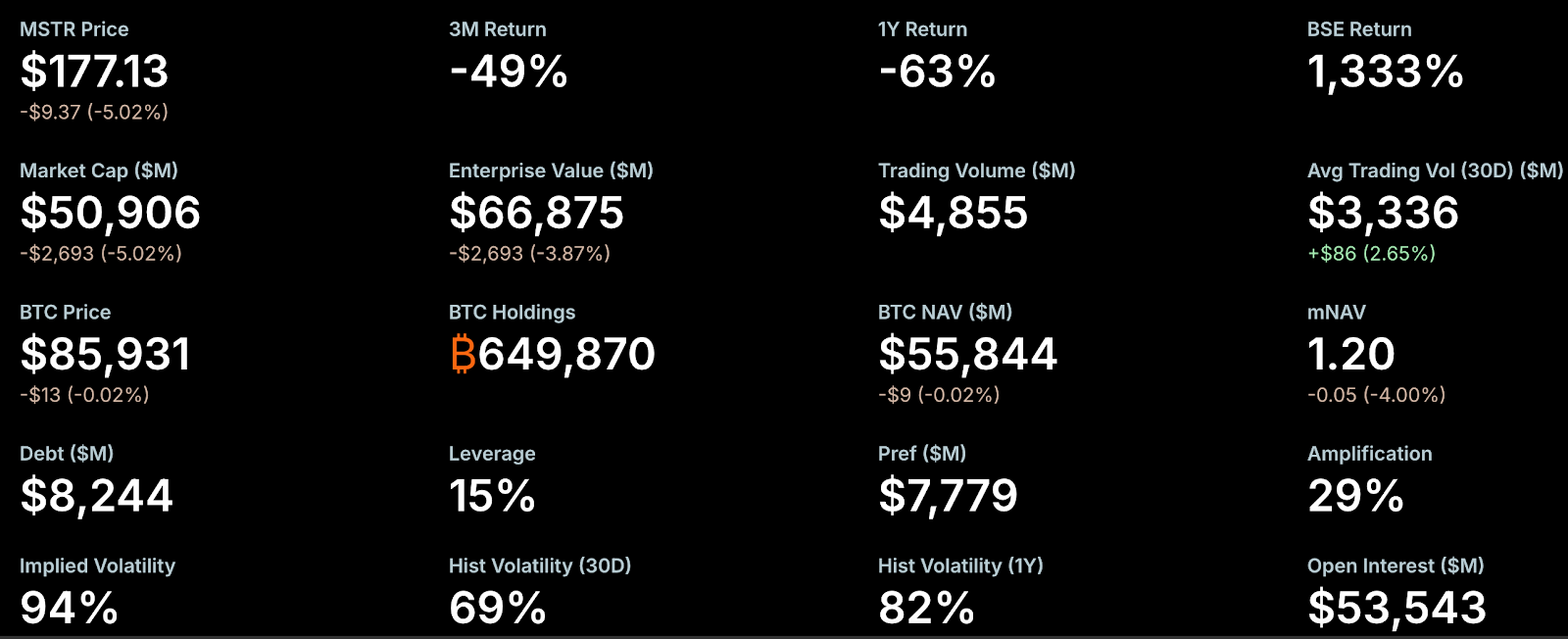

mNAV (market value to net asset value ratio) is a key indicator of market sentiment. Recently, MicroStrategy’s mNAV premium shrank rapidly, coming dangerously close to a critical threshold. According to StrategyTracker, as of November 21, MicroStrategy’s mNAV was 1.2, having previously dipped below 1. This represents a 54.9% drop from its historical peak of 2.66. As the largest and most influential DAT company, the break in MicroStrategy’s treasury premium has triggered market panic. The core issue: a falling mNAV weakens fundraising capacity, forcing the company to issue more shares and dilute existing shareholders, which in turn presses the stock price lower and drags mNAV down further, creating a vicious cycle.

Still, NYDIG’s Global Head of Research, Greg Cipolaro, notes that mNAV has limitations as a metric for DAT companies, and should arguably be removed from industry reports. He argues mNAV may mislead, since it doesn’t account for operating businesses or other assets and liabilities, and is typically based on assumed outstanding shares, excluding unconverted convertible debt.

Sluggish share performance has heightened market concerns. Data from StrategyTracker shows that as of November 21, MicroStrategy’s total market cap (MSTR) was around $50.9 billion—already below the $66.87 billion market value of its nearly 650,000 Bitcoin holdings (average purchase cost: $74,433). That means company shares are trading at a discount to NAV. Since the start of the year, MSTR stock has fallen 40.9%.

This has fueled concerns about exclusion from the Nasdaq 100 and MSCI USA indices. JPMorgan predicts that if MSCI, the global index provider, drops MicroStrategy from its indices, related outflows could reach $2.8 billion; if other exchanges and providers follow, total outflows could reach $11.6 billion. MSCI is now reviewing a proposal to exclude companies whose main business is holding Bitcoin or other crypto assets, and whose digital asset holdings exceed 50% of their balance sheet. A final decision is expected by January 15, 2026.

For now, however, MicroStrategy’s risk of exclusion remains low. For example, the Nasdaq 100 rebalances market cap rankings every December (second Friday), keeping the top 100; ranks 101-125 must have been in the top 100 the prior year, while those below 125 are removed. MicroStrategy remains safely in the top 100, and recent earnings show fundamentals are solid. Institutional investors—including the Arizona State Retirement System, Renaissance Technologies, Florida State Board of Administration, Canada Pension Plan Investment Board, Swedbank, and the Swiss National Bank—disclosed MSTR holdings in Q3 filings, which has also helped support market confidence.

Recently, MicroStrategy’s Bitcoin acquisition rate has clearly slowed, which the market sees as evidence of limited funding—especially since Q3 results showed just $54.3 million in cash and equivalents. Since November, MicroStrategy has added only 9,062 BTC, well below last year’s 79,000 BTC for the same period, though higher Bitcoin prices have also been a factor. This month’s main accumulation was a single big buy of 8,178 BTC last week; other purchases were in the hundreds of coins.

To secure additional funding, MicroStrategy has turned to international markets, launching new financing tools including perpetual preferred shares with high dividends (8–10%). The company recently raised about $710 million by issuing its first euro-denominated perpetual preferred share to back its strategic planning and Bitcoin treasury management program. Notably, the company still has six outstanding convertible bonds, maturing between September 2027 and June 2032.

Insider moves have also drawn attention. MicroStrategy’s earnings report revealed that EVP Shao Weiming will leave on December 31, 2025. Since September, he’s sold $19.69 million in MSTR stock over five trades. These sales were made under a prearranged trading plan under Rule 10b5-1. SEC rules allow insiders to trade under such prearranged plans (with set quantities, prices, or schedules), reducing the risk of insider trading violations.

Analysts Say Debt Risks Are Overblown, High-Premium Investors Under Major Pressure

Amid bearish crypto sentiment and deepening doubts over the DAT model, MicroStrategy founder Michael Saylor reiterated “HODL,” expressing continued optimism despite Bitcoin’s recent drop. He stressed that MicroStrategy won’t sell its Bitcoin unless the price falls below $10,000—reassuring the market.

Meanwhile, analysts have weighed in from several angles. Matrixport notes that MicroStrategy remains a top beneficiary of the current Bitcoin bull run. Earlier, the market worried the company might be forced to sell Bitcoin to repay debts. Based on its current balance sheet and debt schedule, Matrixport sees the odds of “forced Bitcoin sales for debt repayment” as very low in the short term—not a major risk. The most pressure now falls on investors who bought at high premiums. Most of MicroStrategy’s fundraising occurred when its share price was near its all-time high of $474 and net asset value per share was peaking. As NAV fell and the premium compressed, the share price dropped from $474 to $207, leaving high-premium buyers facing major unrealized losses. Relative to Bitcoin’s run-up, MicroStrategy’s stock has pulled back from earlier highs, making its valuation more attractive, and there’s still hope for S&P 500 inclusion in December.

Crypto analyst Willy Woo went further, arguing that MicroStrategy’s debt risks are “highly exaggerated” and that liquidation in a bear market is unlikely. In a tweet, he noted most of MicroStrategy’s debt is in convertible senior notes, which can be repaid in cash, stock, or a mix. MicroStrategy has about $1.01 billion coming due September 15, 2027. Woo estimates that if MicroStrategy’s share price is above $183.19 by then—roughly matching a Bitcoin price of $91,502—it won’t need to sell any Bitcoin to cover the debt.

CryptoQuant founder and CEO Ki Young Ju also views bankruptcy risk as extremely low. He stated, “MSTR would only go bankrupt if an asteroid hit Earth. Saylor would never sell Bitcoin unless shareholders demand it—he’s made that clear many times.”

Ki Young Ju added that even selling a single Bitcoin would undermine MSTR’s identity as a company holding Bitcoin as a primary treasury reserve asset, potentially triggering a reinforcing negative cycle for both Bitcoin and MSTR shares. MSTR shareholders want Bitcoin prices strong and expect Saylor to keep deploying capital allocation strategies so MSTR’s price rises with Bitcoin.

On debt risk, he explained that most of MicroStrategy’s debt is convertible bonds. Failing to reach the conversion price doesn’t equate to liquidation risk; it just means the bonds must be repaid in cash. MSTR has many options for managing upcoming maturities: refinancing, issuing new bonds, securing collateralized loans, or using operating cash flow. Non-conversion doesn’t trigger bankruptcy—it’s just normal debt maturity, not liquidation. While there’s no guarantee MSTR stock will always stay high, the idea that they’d sell Bitcoin to prop up the price or face bankruptcy is baseless. Even if Bitcoin drops to $10,000, MicroStrategy won’t go bankrupt—the worst case would be debt restructuring. MSTR could also use Bitcoin as collateral to raise cash, though that would bring liquidation risk and be a last resort.

Statement:

- This article is reprinted from [PANews] and remains the copyright of the original author [Nancy]. If you have concerns about this reprint, please contact the Gate Learn team for prompt handling per our procedures.

- Disclaimer: The views and opinions in this article are solely those of the author and do not constitute investment advice.

- Other language versions of this article are translated by the Gate Learn team. Do not copy, distribute, or plagiarize these translations without referencing Gate.

Share

Content

Related Articles

The Future of Cross-Chain Bridges: Full-Chain Interoperability Becomes Inevitable, Liquidity Bridges Will Decline

Solana Need L2s And Appchains?

Sui: How are users leveraging its speed, security, & scalability?

Navigating the Zero Knowledge Landscape

What is Tronscan and How Can You Use it in 2025?